Executive Summary

Marketing got the biggest share of enterprise AI budgets first, and now it has to prove what that money bought. That is the shift this edition reads. Open Future Forum's CFO AI Leverage Report followed the money to the CFO. This report follows it to the seat that spends more of it on AI than any other operating function and is under the most pressure to show it paid: the CMO.

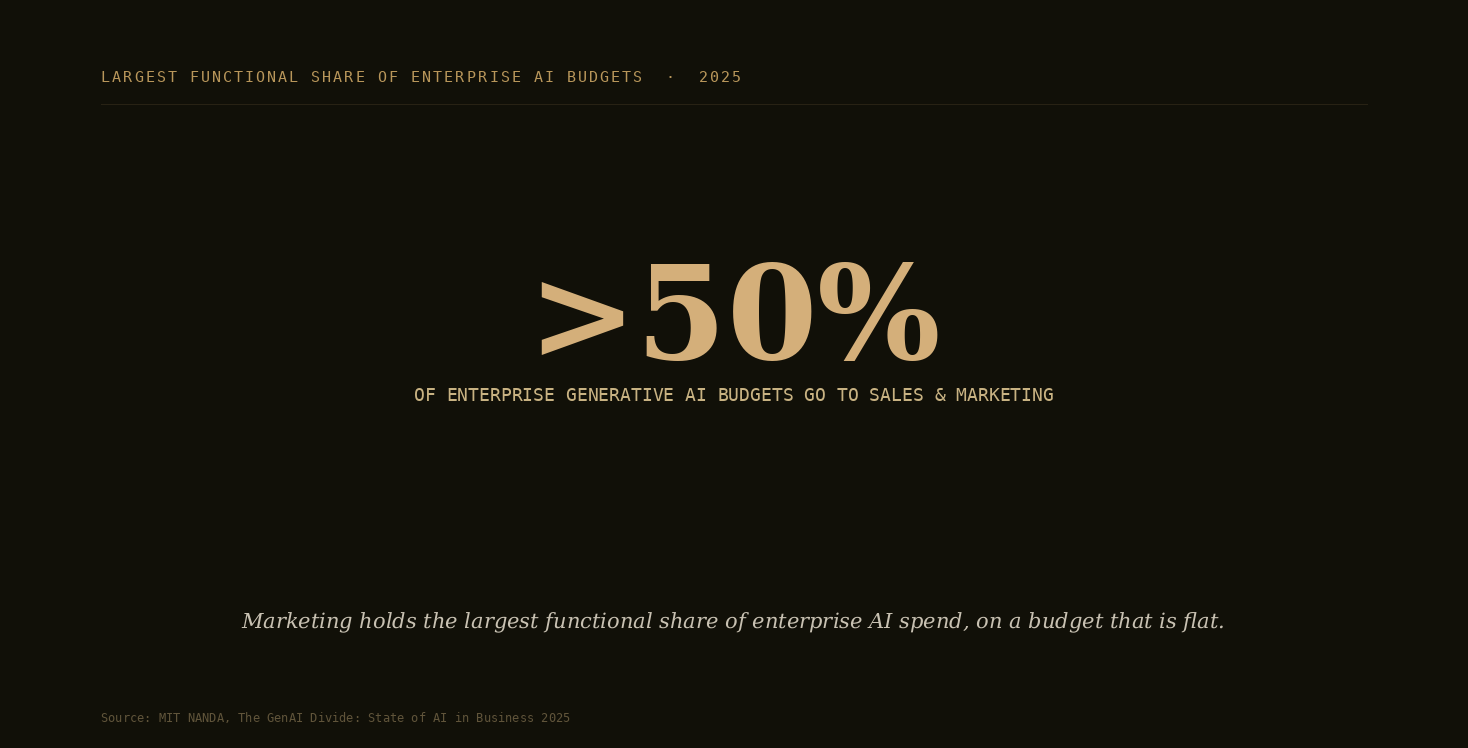

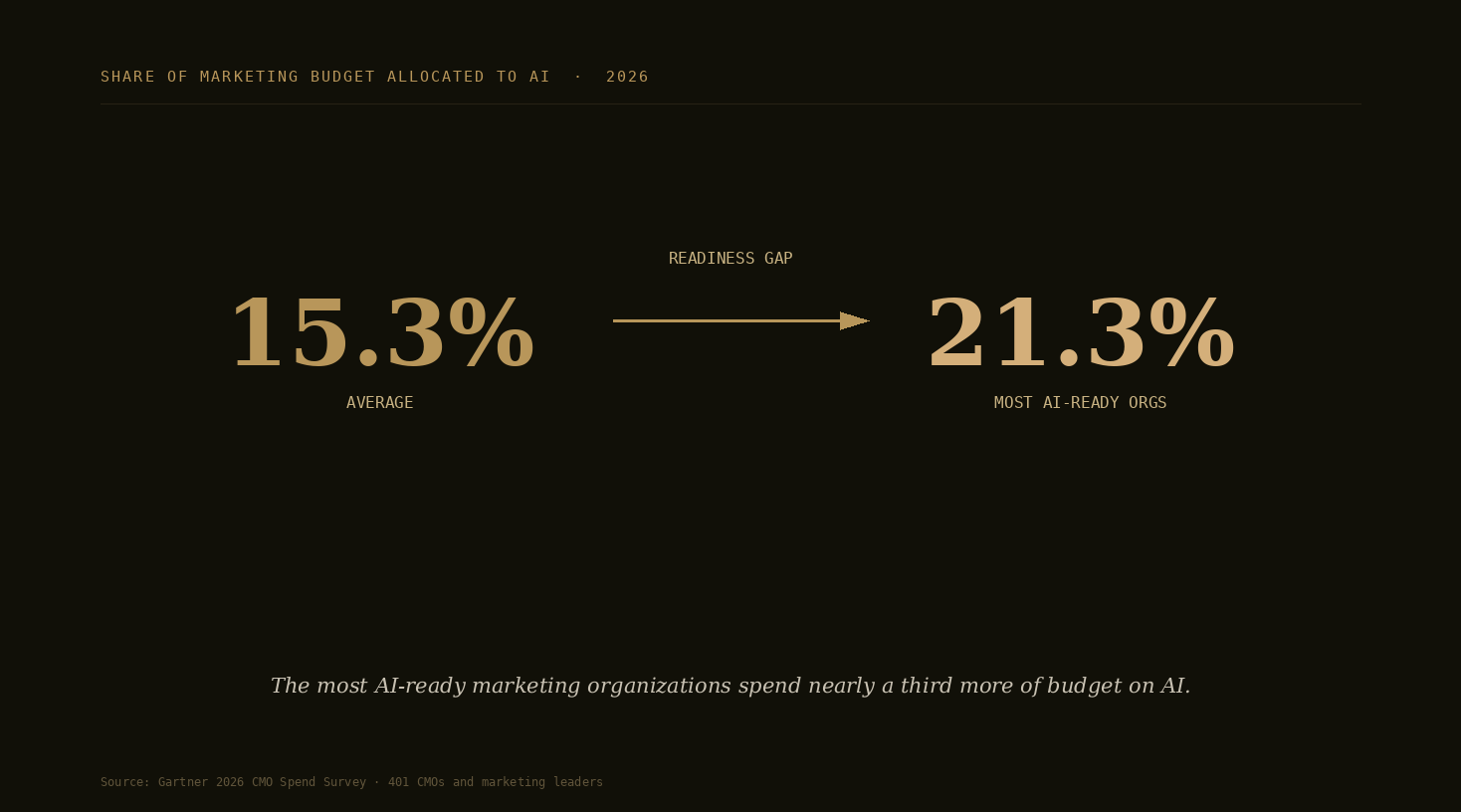

The external picture is stark on both sides. MIT research has found that more than half of enterprise AI budgets flow to sales and marketing, the largest functional share. At the same time, Gartner's 2026 CMO Spend Survey of 401 marketing leaders found CMOs allocating about 15.3 percent of marketing budgets to AI while only 30 percent report mature AI readiness, and overall marketing budgets sit effectively flat at 7.8 percent of company revenue. Read together: marketing holds the largest AI budget of any function, the budget around it is not growing, and most marketing organizations admit they are not yet built to scale what they bought.

This report reads that shift from inside the room. Its flagship metric, the CMO AI Leverage Index, measures the share of marketing leaders who say AI now lets marketing grow output without growing headcount, agency spend, or budget. In marketing, agency and contractor spend is the second form of headcount, so the instrument asks about it explicitly.

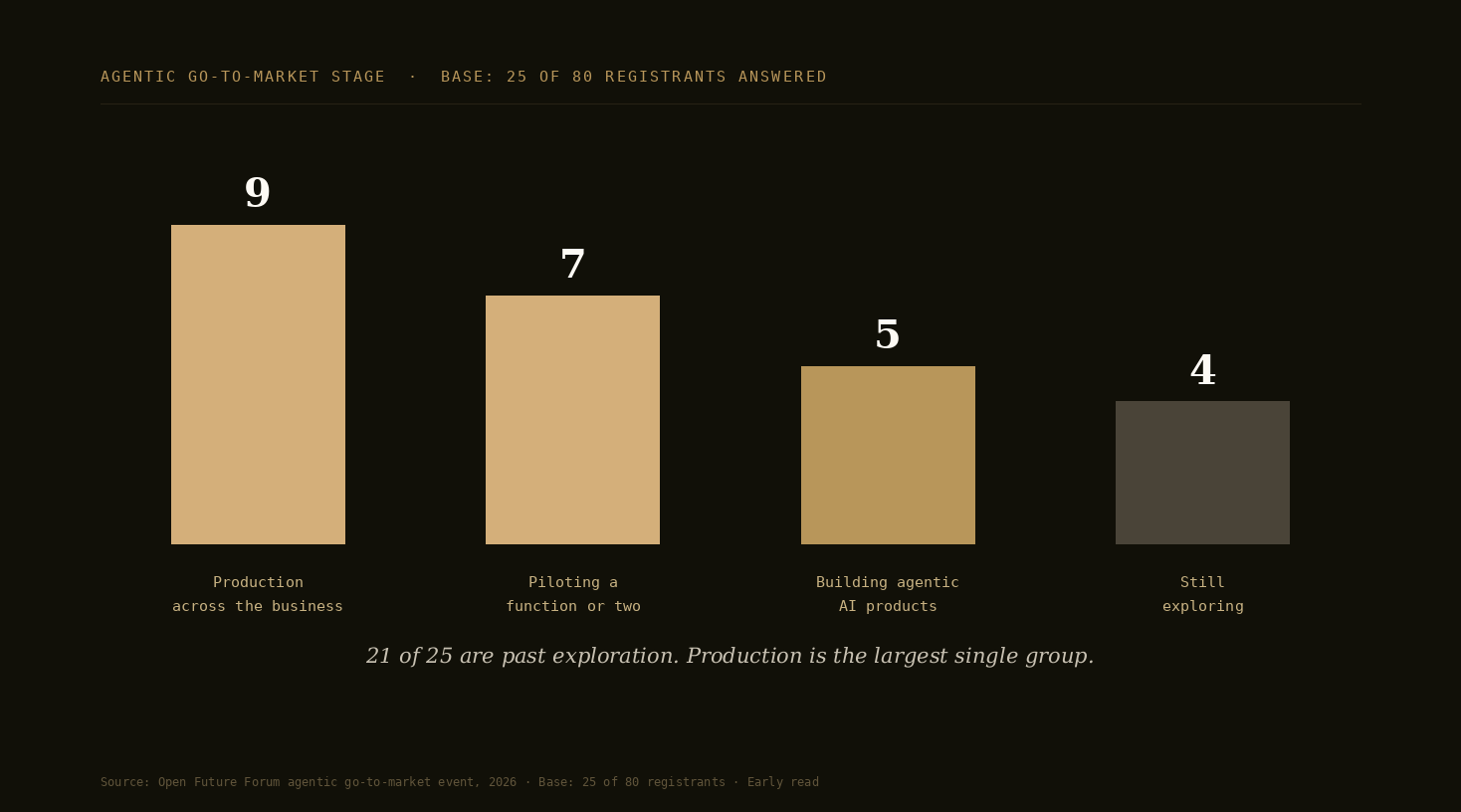

The early signal from Open Future Forum's own rooms already points in two directions at once, and both are in this report. From the CMO room: content speed and customer insight tie at the top of where AI helps most, and two of the seven marketers we asked also named doing the work of more people, the first appearance of the headcount-leverage story in the marketing lane. From the agentic go-to-market room: 21 of the 25 registrants who answered the stage question are past exploration with agents, nine of them running agents in production across the business. And from the supply side, a finding that frames the whole edition: of the sixteen AI founders we asked who owns the buying decision inside the companies they sell to, not one named the CMO. These are early reads on small bases, reported as what they are, and they firm up edition over edition as the responses grow.

The Answers We Have Now

This section is the data in hand. It is drawn from Open Future Forum event registration records across more than 20 events in 2026, more than 200 executive registrations in total, read here for the marketing and growth lane, plus the first responses to the instrument questions now embedded in the registration flow. Figures are reported as rounded floors of distinct registrants, with the response base stated on every early read. They describe demand, composition, and first opinions. Spend figures arrive as the instrument bases grow.

Registration forms collect screening data, and only the newer instrument questions collect opinion. So the counts tell us who is being pulled toward which AI question, and the instrument answers, still on small bases, tell us what those people think in their own words.

Finding 1: The marketing lane is the smallest of the operating lanes, and the furthest along the agent curve

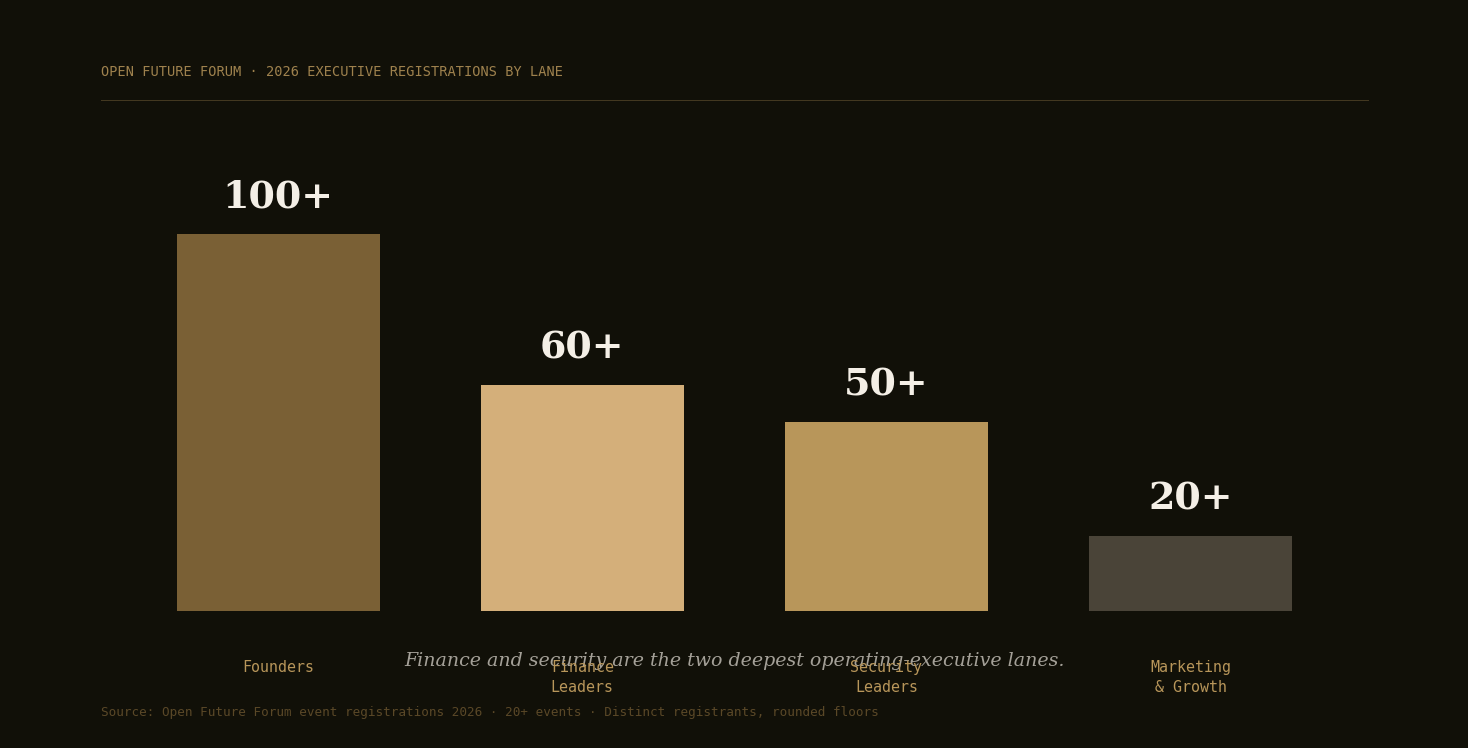

Across 2026, the Open Future Forum lanes rank: more than 100 founders, more than 60 finance leaders and operators, more than 50 security leaders, and more than 20 marketing and growth leaders. Marketing is the thinnest operating-executive lane in our rooms. It is also, on the first stage data, the most agentic. At the agentic go-to-market event, 25 of the 80 registrants have answered the stage question, and 21 of those 25 are past exploration: nine running agents in production across the business, seven piloting agents in a function or two, five building agentic AI products, and four still exploring. Production is now the largest single group. The lane is small. The people in it are not early.

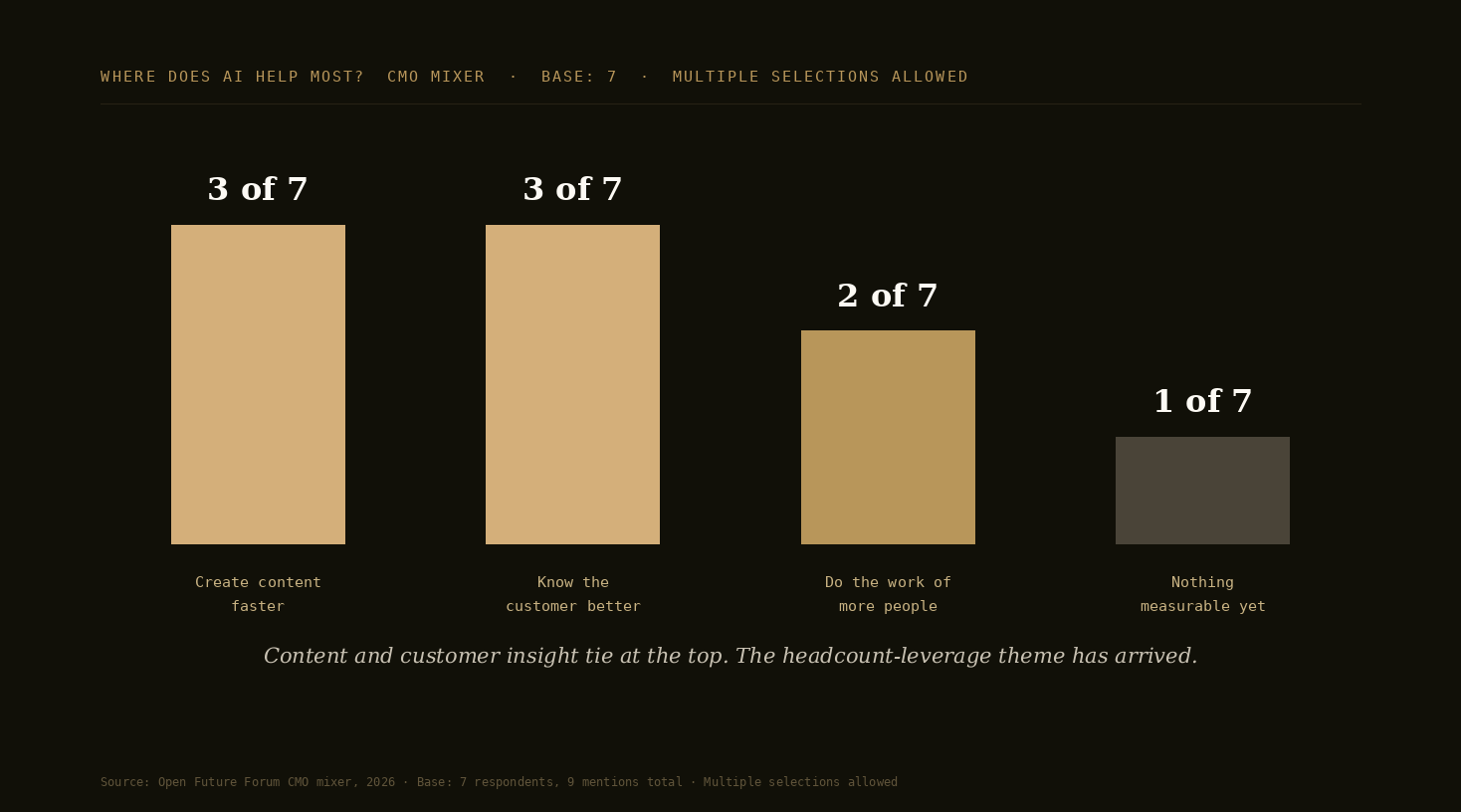

Finding 2: Content speed and customer insight lead, and the do-more-without-hiring theme has arrived

Among the marketers we asked where AI helps most, creating content faster and knowing the customer better tie at the top, each named by three of seven. Two of the seven also chose doing the work of more people. One said nothing measurable yet. That distribution is the marketing lane in miniature: AI reads first as a quality-and-speed play, the cost-out story is beginning to show up, and the skeptic is in the room too. The two of seven naming headcount-style leverage is the seed reading of the CMO AI Leverage Index, and it is the line this report will track edition over edition.

Finding 3: What marketers are building is a full-stack content and pipeline engine, and they are already optimizing for AI answers

Asked what they are working on right now that AI touches, the go-to-market room answered in a consistent shape: campaigns, lifecycle marketing, cold outreach, content ideation, strategy and planning, prospecting, video production, a content engine, agentic commerce and workflows, automated brand review. One answer stands out for what it says about where marketing attention is going: one registrant named GEO, generative engine optimization, alongside agent experience. Marketers in this room are no longer only optimizing for search. They are optimizing for the answers AI engines give, which means the discipline this lane invented for Google is being rebuilt for AI, and the people rebuilding it are sitting at these tables.

Finding 4: What the room asks for is proof and guardrails, not inspiration

The open-text answers to what registrants want to walk out with cluster tightly: checks and balances for agents, where AI creates leverage and where it fails, real-world failure modes, bottlenecks and their solutions, a sample marketing agentic flow that is actually in production, how other teams are using agents in go-to-market, the current state of the art in AI go-to-market, a concrete list of agents that help with sales and marketing demand, what brands are struggling with, and what is working well. Nobody asked for a vision talk. The room is asking for evidence, controls, and a shortlist, which is exactly what a buyer sounds like the year the pilots come due.

Three honesty notes on the counts

- The instrument questions were added partway through registration at both the CMO mixer and the go-to-market event, so only later cohorts answered them. That is why the bases are 7 and 16 against much larger registrant counts, and why every early read carries its base on its face.

- The CMO rooms are role-mixed. The seven respondents span a GTM director, a partnerships director, a programs lead, a founder-CEO, a PR vice president, and a software engineer. So "marketing leaders" is defensible; "seven CMOs" overstates it, and we do not say it.

- "Surveyed" applies only to the instrument answers. The registration counts are screening data. Accurate verbs for those: convened, brought together, engaged.

Defensible claim language, from the data in hand

- "In 2026, Open Future Forum convened 200+ executive registrations across 20+ events, including 20+ marketing and growth leaders alongside 60+ finance leaders and 50+ security leaders."

- "In the Open Future Forum go-to-market room, 21 of the 25 registrants who answered the stage question are past exploration with AI agents."

- "Among the marketers Open Future Forum asked, creating content faster and knowing the customer better tie as the places AI helps most, and two of seven named doing the work of more people."

- "Of sixteen AI founders asked who owns the buying decision inside the companies they sell to, not one named the CMO."

The instrument is live across the marketing, finance, security, and founder rooms, and the first answers are arriving with every event. In the marketing lane, the where-AI-helps and agentic-stage questions are returning the cleanest early signal, and the attribution and agency-spend questions enter the field at the next CMO Executive Forum gathering. The next edition reports each on a larger base, filtered to marketing leaders, with percentages of those who answered. Read the figures in this edition as the first data points on a line we will track, not as settled numbers.

By the Numbers

The marketing AI shift, in the figures the market is citing in 2026. External benchmarks are attributed to their sources. The Open Future Forum figures are early reads from our own rooms, with the base shown.

- More than half of enterprise AI budgets go to sales and marketing, the largest functional share (MIT).

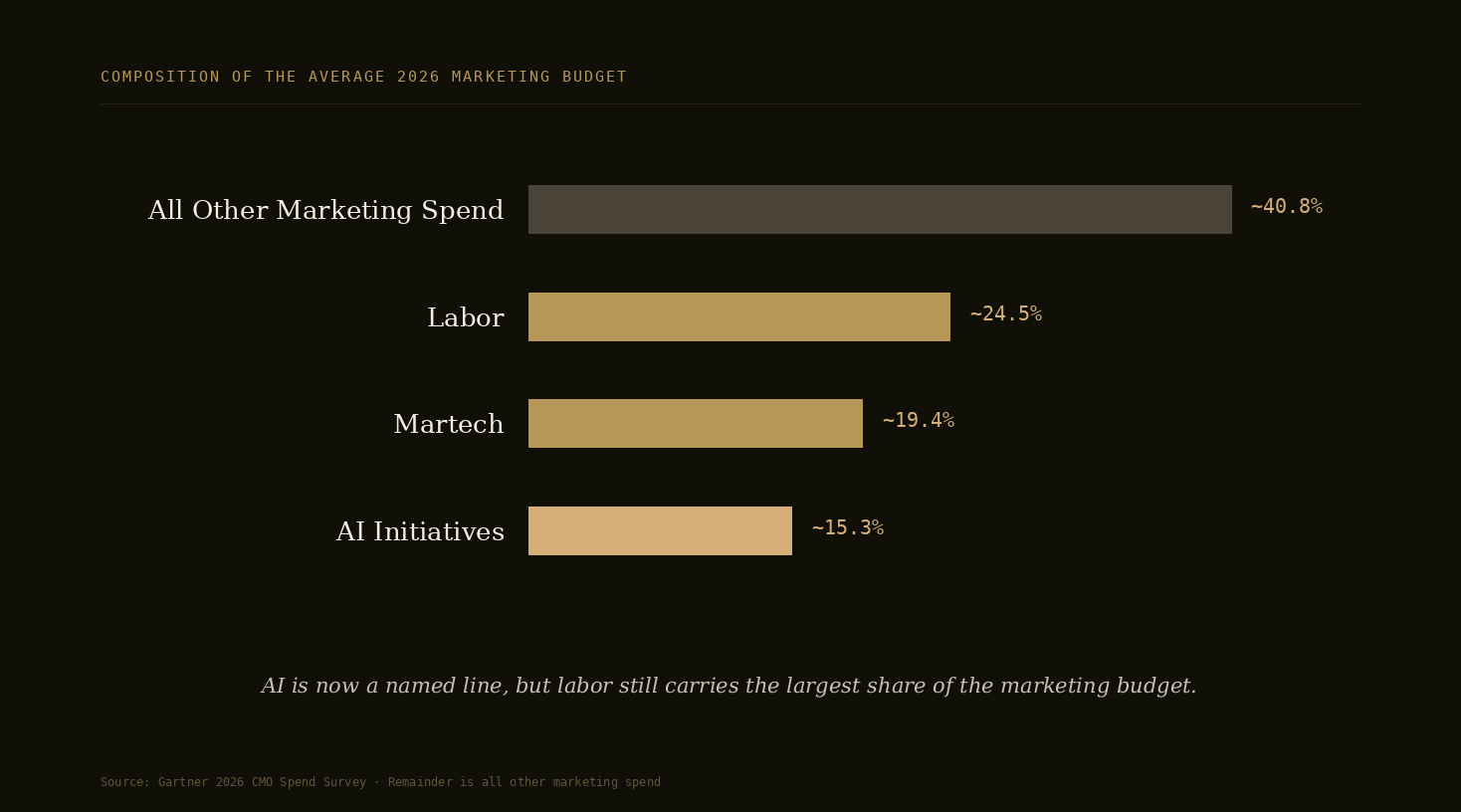

- 15.3 percent of marketing budgets now go to AI initiatives on average, rising to 21.3 percent among the most AI-ready marketing organizations (Gartner 2026 CMO Spend Survey, 401 marketing leaders).

- 70 percent of CMOs call becoming an AI leader a critical 2026 goal, while only 30 percent report mature AI readiness and 70 percent say their internal processes are not yet mature enough to scale AI (Gartner).

- 7.8 percent of company revenue is the average 2026 marketing budget, effectively flat year over year, and 56 percent of CMOs say they lack the budget to deliver their 2026 strategy (Gartner).

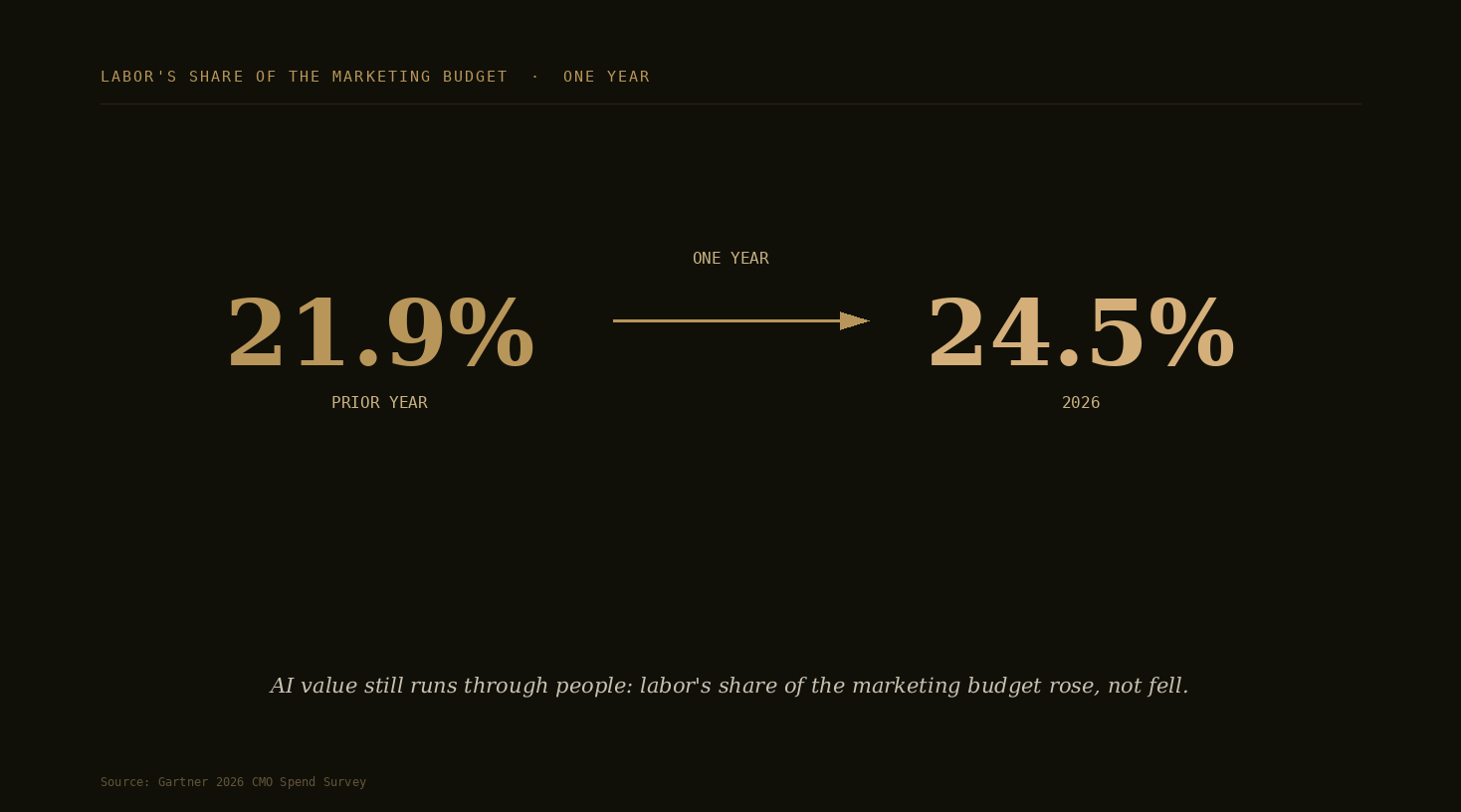

- 24.5 percent is where labor's share of the marketing budget moved in one year, up from 21.9 percent, evidence that AI value still runs through people and skills (Gartner).

- 56 percent of CMOs increased the share of their martech budget on consumption or usage-based pricing in the past year, while martech's overall share of marketing budgets hit a five-year low of 19.4 percent (Gartner, reported by Chief Marketer).

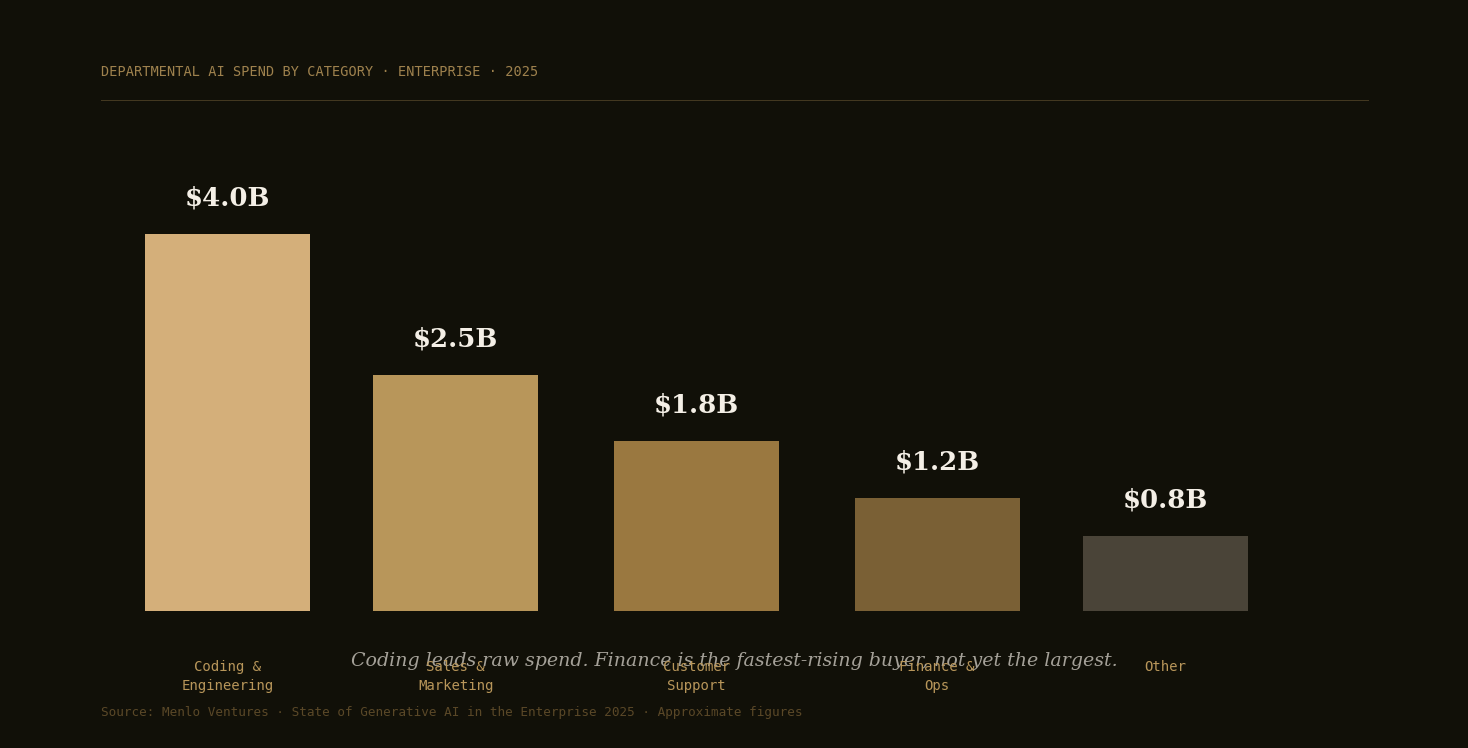

- The largest line in raw departmental AI spend still belongs to coding, the honest counter to any single-function story (Menlo Ventures).

From our own rooms, early reads with the base shown:

- 3 of 7 marketers named creating content faster, 3 of 7 named knowing the customer better, and 2 of 7 named doing the work of more people (Open Future Forum CMO mixer, base of 7, multiple selections allowed).

- 21 of 25 registrants in the go-to-market room are past exploration with agents, nine of them in production across the business (Open Future Forum, base of 25).

- 0 of 16 founders named the CMO as the owner of the buying decision they sell into. They named the CIO, the CTO, and the business unit instead, and about 7 in 10 of those charging price on usage or outcomes (Open Future Forum founder events, base of 16).

The Thesis, in One Line

Marketing took the largest share of enterprise AI budgets before any other function, on a budget that is not growing, and the deciding question for the CMO has moved from what AI can make to what marketing can stop paying for. This Report puts a measured number on that, from the room where it is being decided.

What CMOs Are Saying, and What Sellers Are Saying

This is the edition's core, and it is deliberately two-sided. The buyer side is the marketing leaders in the Open Future Forum rooms, answering in their own words. The supply side is the founders building and selling AI into the enterprise, answering who actually buys from them and how they charge. The gap between the two sides is the sharpest finding in this edition.

The buyer side: what the CMO room says

Where AI helps most, in their words and their counts: creating content faster and knowing the customer better tie at the top, three of seven each. Doing the work of more people is second, two of seven. Nothing measurable yet, one of seven. So marketing AI still reads first as a quality-and-speed play, but the cost-out reading has arrived, and the honest skeptic is at the same table.

What blocks them, in their words: data. Asked their biggest marketing challenge, one GTM director answered with a single word, data, which matches Gartner's finding that a lack of integrated marketing data is the second most cited barrier to AI-driven marketing efficiency. A founder-CEO in the room asked why marketing and sales are not one team, which is the organizational version of the same problem: agents do not respect the wall between the two functions, and the pipeline they automate runs straight through it. A third named brand adoption, the question of how a brand gets chosen at all when an AI answer engine sits between the customer and the shelf. Three answers, three layers of the same shift: the data layer, the org layer, and the demand layer.

And what they want next, from Finding 4: checks and balances for agents, evidence of where AI creates leverage and where it fails, and a concrete shortlist. That is a buyer preparing to consolidate, not someone collecting pilots.

The supply side: what the sellers say

Of the sixteen AI founders we asked who owns the buying decision inside the companies they sell to, not one named the CMO. They named the CIO and CTO, the business unit, and bottom-up adoption. The closest any answer comes to marketing is the business unit, which can contain it but does not name it. And of the founders charging, about 7 in 10 price on usage or outcomes rather than per seat.

Here is why that pricing detail matters more than it looks. Gartner reports that 56 percent of CMOs increased the share of their martech budget on consumption-based pricing in the past year, and that half of the organizations using those models are continually renegotiating contracts to control usage spikes. The sellers' pricing model and the buyers' budget model are converging on the same shape, usage and outcomes, even while the two sides do not yet name each other. When a vendor charges per outcome, marketing attribution stops being a dashboard and becomes the contract. The function that owns attribution is marketing. Which means the CMO becomes the buyer of record whether or not the seller has named the seat yet.

What the Marketing Seat Sees Across the C-Suite

Marketing AI does not stay in marketing. It is approved by finance, deployed through IT, secured by the CISO, and judged by the CEO on a growth number. That gives the marketing seat a view of the whole C-suite, and it gives every other seat a view of marketing. What follows is that view, seat by seat, read from the marketing side and written that way on purpose. External figures are attributed; the rest is what our own rooms say.

The CEO

BCG's AI Radar 2026 found 72 percent of CEOs calling themselves the main AI decision-maker, double the prior year. From the marketing seat the CEO sets the AI ambition and the growth target in the same breath, and the CMO is asked to hit both without new budget. Gartner found 62 percent of CMOs expect budget cuts if 2026 growth targets are missed, which is that pressure stated as a number.

The CFO

The CFO AI Leverage Report found the finance seat sees marketing as the fastest AI tool sprawl and the hardest attribution: easy to start, hard to measure. On a flat 7.8 percent budget, every marketing AI line now has to survive a finance review. The CMO who arrives with cost per outcome rather than cost per impression is speaking the language the CFO AI Leverage Report documented.

The CIO

The seat the founders actually sell to, nine mentions of sixteen in our founder room. As martech shifts to consumption pricing and agents touch core systems, the CIO's stack decisions increasingly determine what marketing can deploy, which puts the CMO and the CIO inside the same purchase whether they plan it or not.

The CRO and the sales line

The question from our own room, why are marketing and sales not one team, is where agentic go-to-market lands hardest. An agent that runs prospecting, outreach, and content in one loop does not stop at the MQL handoff, and the org chart will have to answer for that before the tooling does.

The CISO

Marketing agents act in public, in the brand's voice, on customer data. That makes marketing the function where an agent failure is a headline rather than an incident report. The go-to-market room's own first ask, checks and balances for agents, is the CISO's agenda in the CMO's own words, and it is why the Open Future Forum marketing and security lanes increasingly share a table.

The CAIO and the AI leader

Where the seat exists, marketing is usually its biggest internal customer, because marketing holds the largest functional share of the AI budget (MIT). From the marketing seat the CAIO is an ally on governance and a rival on ownership, and which one wins depends on who is accountable for the growth number.

The agency

Marketing's counterparty no other function has. Agency and contractor spend is marketing's second labor line, and it is where the leverage question lands first: content, creative iteration, and media operations are the work AI absorbs earliest. The CMO AI Leverage Index asks about agency spend explicitly for exactly this reason.

The venture investor

The capital consensus for 2026 is concentration: more spend through fewer vendors. For marketing that means the tool sprawl the CFO AI Leverage Report documented is ending from the supply side too, and the martech share of marketing budgets hitting a five-year low of 19.4 percent (Gartner) is the same consolidation read from the buyer side.

The founder

The supply side of this edition. Not one of sixteen named the CMO as their buyer, and about 7 in 10 of those charging price on usage or outcomes. Read from the marketing seat, that is not absence, it is approach: outcome pricing makes attribution the contract, and attribution belongs to marketing.

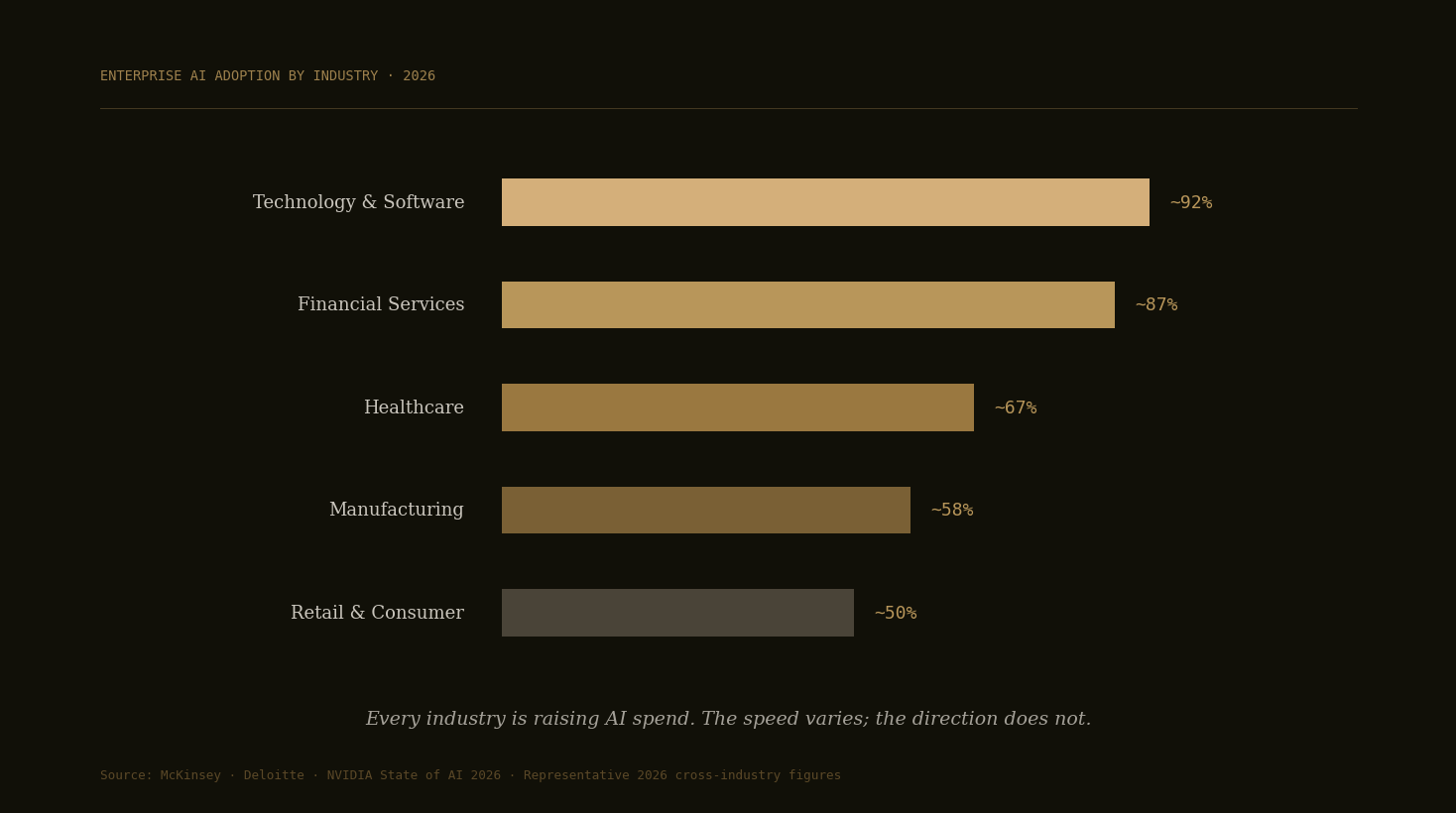

The Same View, by Industry

Industry sits underneath all of this, because a CMO at a bank and a CMO at a retailer are funding very different AI. Open Future Forum does not yet run industry-specific CMO rooms, so this read is drawn from external benchmarks rather than our own data, and it is written as the marketing-seat view of where each sector's spend is going. The adoption figures are representative of 2026 cross-industry surveys and are attributed to McKinsey, Deloitte, and NVIDIA, consistent with the CFO AI Leverage Report.

Technology and B2B software

The highest adopter, around 92 percent, and the home of our own go-to-market room. This is where agentic go-to-market is furthest along: prospecting, outreach, content, and pipeline in one loop. The marketing question here is not whether to use agents but how to govern them, which is exactly what the room asked for.

Retail and consumer

Among the highest adopters of agentic AI, close to half of firms, with the value in personalization, demand forecasting, and inventory. This is the sector where the brand-adoption question from our own room lands hardest: when an AI answer engine sits between the customer and the shelf, being the answer becomes the marketing job. From the marketing seat, retail is where AI touches revenue most directly, so the growth case leads and the cost-out case follows.

Financial services

Around 85 to 89 percent adoption on Deloitte's numbers, and the most compliance-gated marketing in the economy. Every AI-generated claim passes a review that was built for humans, so the marketing AI that wins here is the kind that carries its audit trail with it. The leverage is real, but it arrives through governance, not around it.

Healthcare and life sciences

The fastest accelerator, climbing from roughly 38 percent adoption in 2024 to about 67 percent in 2026 as regulatory clarity arrived. Marketing here is regulated speech: claims, indications, and consent. The near-term marketing AI value is administrative, content operations and documentation, the same pattern the CFO AI Leverage Report found in healthcare overall.

Manufacturing and industrials

Slower to adopt, around half to two thirds of firms, and the sector where marketing AI reads most like sales enablement: long cycles, technical content, channel partners. The cleanest early leverage is content and translation at scale for global channels, and it is measurable, which is how this sector funds things.

The pattern across all five is the one this Report measures. Where marketing output is measurable, AI is funded fast. Where the measure is brand, the CMO is still building the case. The industry does not change the question. It changes how quickly the answer comes.

What Marketing People Say About the Spend

The buyer side of this report is the CMO funding AI. The commentary around that spend has split into a sharp, useful debate in 2026, and a buying-and-budget report has to carry both sides.

The reckoning

The skeptic case runs through three claims, and each has teeth. First, output without outcomes: AI has made content cheap to produce, and cheap content floods every channel, so the marketers winning are the ones spending the savings on distinctiveness rather than volume. The one respondent in our own room who answered nothing measurable yet is this case in person. Second, the readiness gap: Gartner's finding that 70 percent of CMOs say their processes are not mature enough to scale AI means most of the 15.3 percent being spent is running ahead of the discipline around it, the same pattern MIT documented across enterprise pilots generally. Third, the labor paradox: labor's share of marketing budgets rose from 21.9 to 24.5 percent in a year, so the function buying AI to need fewer people currently needs more skilled ones.

The counter-case

The bull case is that marketing is where AI's return shows up first because marketing output is already measured in market terms. Content, personalization, and demand generation produce numbers weekly, not quarterly, which is why generative AI for content and personalization was the transformation CMOs most expected to yield cost-efficiency results this year (Gartner). The most AI-ready marketing organizations are already spending 21.3 percent of budget on AI against the 15.3 percent average, and reporting bigger overall budgets, which reads as AI maturity earning budget rather than consuming it. And the agentic front of the lane, 21 of 25 past exploration in our own room, is not waiting for the readiness surveys to catch up.

Why it matters for this report

The two sides are not actually in conflict, and the reconciliation is the point. Spend is flat overall and concentrating on what proves out, which is what a market does when the buyer starts answering for return. The reckoning is the proof gate closing. The counter-case is the leaders passing through it. The CMO AI Leverage Index measures who is getting through, edition over edition, from inside the rooms where the question is being decided.

The Evidence Behind the Theses

The Report rests on five theses. Here is how each holds up against outside data from 2025 and 2026, the support and the counter-evidence, so the claims are calibrated rather than asserted. External figures are attributed to their sources and used for context. They are not Open Future Forum findings.

Thesis 1: Marketing holds the largest functional share of enterprise AI spend. Well supported, stated carefully.

Support. MIT research found more than half of enterprise AI budgets going to sales and marketing, the largest functional share. Gartner's 2026 CMO Spend Survey found CMOs allocating 15.3 percent of marketing budgets to AI on average, with the most AI-ready organizations at 21.3 percent.

Counter, and this is the honest part. On raw departmental application spend, coding leads in Menlo Ventures' taxonomy. The reconciliation is definitional: sales and marketing lead as a combined functional share of total AI budgets, while coding leads as a single application category. The Report states it that way.

Thesis 2: The CMO buys on proof inside a flat budget. Well supported.

Support. Gartner found marketing budgets effectively flat at 7.8 percent of company revenue, 56 percent of CMOs saying they lack the budget for their 2026 strategy, and 62 percent expecting budget cuts if growth targets are missed, which makes every AI line a survival test. Martech's share of marketing budgets hit a five-year low of 19.4 percent even as 62 percent of CMOs planned to invest more in marketing technology, meaning fewer, harder-working tools. Our own room says the same in its own words: the walk-out-with answers were evidence, controls, and a shortlist.

Counter. The pressure to show AI leadership, 70 percent of CMOs calling it a critical goal, can push spend ahead of proof, and Gartner's finding that only 30 percent report mature AI readiness suggests much current spend is still ahead of the discipline around it.

Thesis 3: AI is beginning to decouple marketing output from headcount and agency spend. Early, and the counter-evidence is real.

Support. Two of the seven marketers we asked already name doing the work of more people as a place AI helps most, and generative AI for content creation and personalization was the transformation CMOs most expected to yield cost-efficiency results this year in Gartner's survey. Gartner also frames the CMO mandate in 2026 as delivering growth, efficiency, and transformation without meaningful budget expansion, which is the leverage mandate by another name.

Counter. Labor's share of the marketing budget rose from 21.9 percent to 24.5 percent in a year, and the most cited barrier to AI-driven marketing efficiency is a lack of internal talent. The leverage is real where it lands, but so far AI in marketing is adding skilled people even as it promises to need fewer, which is exactly why the CMO AI Leverage Index is worth measuring rather than assuming.

Thesis 4: Agentic go-to-market is running ahead of the maturity the surveys assume. First-party, early, treated as a directional signal.

Support. 21 of the 25 registrants in our go-to-market room who answered the stage question are past exploration, nine in production across the business, the largest single group. The room's questions, checks and balances for agents, where AI fails, are post-deployment questions.

Counter. The base is 25, self-selected into an agentic event, so it describes the leading edge, not the market. Gartner finds 70 percent of CMOs saying their processes are not mature enough to scale AI, and separately expects a large share of agentic projects to be canceled before 2028. We carry this thesis as what it is: the front of the curve, measured, with the rest of the curve behind it.

Thesis 5: Answer engines are becoming a marketing channel CMOs actively optimize for. Early, treated as observation.

This is the softest of the five, and it is presented as a pattern rather than a measured shift. The supporting signal is small and first-party: a registrant in our own go-to-market room named GEO, generative engine optimization, as live work, and the brand-adoption challenge named in the CMO room is the same question from the demand side. Against it, no major 2026 marketing survey yet tracks answer-engine optimization as a budget line. So the Report carries this as an emerging observation about where marketing attention is going, adds an answer-engine question to the rotating instrument, and lets the data decide in later editions.

About This Report

The CMO AI Leverage Report is a standalone Open Future Forum research report. It reads how the marketing leaders who hold AI budgets are buying, funding, and getting leverage from AI, from the operator level, wherever Open Future Forum convenes them. This is Edition 1, and each edition carries its own number so the CMO AI Leverage Index line can be tracked over time. The Report does not claim to size the enterprise AI market, and no single figure in it is presented as a market estimate.

Two companion Open Future Forum reports stand alongside this one, each standalone. The CFO AI Leverage Report reads finance. The Executive AI Leverage Report reads the leverage itself across all the rooms, on the Executive AI Leverage Ladder. The three share the same community, the same honesty rules, and the same base-on-face convention, and they cite each other where the lanes cross.

What This Is

The CMO AI Leverage Report is a recurring read on one question, asked of the marketing leaders in the Open Future Forum community: is AI letting your marketing function do more without adding headcount, agency spend, or budget, and how are you funding it.

It is built on a base most people cannot reach. Open Future Forum runs the CMO Executive Forum and the CMO Dinner Series, invitation-screened gatherings where the same marketing leaders return event after event, which means their answers can be collected directly and tracked over time. That is the asset. This Report reads it.

The flagship number is the CMO AI Leverage Index: the share of marketing leaders who say AI now lets them grow marketing output without growing the team or the agency line. Budget-share figures belong to Gartner. The leverage read, from marketing operators, tracked over time, belongs to no one yet.

What This Is Not

This is the honest part, and it is what keeps the Report credible. This is not a market-size estimate. It does not compete with the Gartner CMO Spend Survey, which reads 401 marketing leaders at mostly billion-dollar companies and does it well. This Report reads a single question from inside one room, the Open Future Forum marketing community, a selective sample of operators. Early editions are directional, the response base is stated on every figure, and nothing here is presented as a probability sample of all marketing organizations. The value is not scale. The value is that these are actual operators, answering in their own words across editions, so the line can be tracked.

The Gap It Fills

The big surveys say marketing spends the most on AI and trusts it the least in its own readiness. What none of them reads is the leverage itself, at the operator level, on the headcount-and-agency question specifically, tracked over time in the same community. The macro names the pressure. This Report measures the response, among marketing leaders deciding in real time whether AI changes their hiring plan and their agency roster. It sits next to the big surveys, not against them.

Definitions

- Marketing leader. A respondent who owns or directly influences the marketing AI budget: CMO, VP Marketing, head of growth, head of demand or GTM, or a founder acting as head of marketing. Answers from advisors, vendors, and non-marketing roles are recorded separately and not counted in headline figures.

- Marketing AI budget. Money the marketing function commits over 12 months to generative or agentic AI: martech tooling, internal build, agency and outside services with an AI component, and supporting data. It excludes general martech that predates AI work.

- Headcount-and-agency leverage. Using AI to raise marketing output without a matching rise in headcount or agency spend. The flagship metric measures it. Agency spend is included because it is marketing's second labor line.

- Respondent base. Every published figure states the number of marketing leaders behind it. No headline figure is published below 40 responses; smaller bases are labeled early reads.

Questions This Report Answers

What is the CMO AI Leverage Index?

The CMO AI Leverage Index is an Open Future Forum metric: the share of marketing leaders who say AI lets marketing grow output without growing headcount or agency spend. It is the flagship measurement of the CMO AI Leverage Report and is tracked edition over edition.

Who actually buys marketing AI?

Today, mostly not the CMO. Of sixteen AI founders Open Future Forum asked, not one named the CMO as their buyer; they named the CIO, the CTO, and the business unit. But with about 7 in 10 charging founders pricing on usage or outcomes, and 56 percent of CMOs shifting martech budget to consumption pricing (Gartner), the buying decision is converging on the seat that owns attribution: the CMO.

How much of marketing budgets goes to AI in 2026?

About 15.3 percent on average, rising to 21.3 percent among the most AI-ready marketing organizations, on overall marketing budgets that are effectively flat at 7.8 percent of company revenue (Gartner 2026 CMO Spend Survey).

Is AI replacing marketing headcount?

Not yet at scale. Two of the seven marketers Open Future Forum asked named doing the work of more people as a place AI helps most, an early read, while Gartner finds labor's share of marketing budgets actually rising, from 21.9 to 24.5 percent. The leverage is arriving; the CMO AI Leverage Index exists to measure when it lands.

What is the CMO Executive Forum?

The CMO Executive Forum is Open Future Forum's gathering program for marketing and growth leaders, run alongside the CMO Dinner Series as small, off-the-record dinners for C-suite executives in Silicon Valley. It is where the instrument behind this report is fielded.

What We Will Measure

The answers in hand today are demand, composition, and first opinions. The Report is built to add the spend layer, collected from marketing leaders through a short instrument, fielded first at the next CMO Executive Forum gathering and then at every CMO Executive Forum and CMO Dinner Series event. These figures are not inferred from registrations. They come from a question an executive answered.

The Flagship Metric: the CMO AI Leverage Index

Question (marketing leaders only): In the function you lead, AI is mainly used to: do more without adding headcount or agency spend / replace planned hires or agency work / free existing staff for higher-value work / not yet material.

The Index is the combined share choosing the first two answers, the marketing leaders for whom AI has changed the hiring or agency math. It is reported as a single percentage with the full distribution beneath it, and it is the line tracked edition over edition. The seed reading is already in hand: two of seven at the CMO mixer, an early read, base on its face.

Core (every edition, marketing leaders only)

- Headcount-and-agency leverage (the flagship question above).

- Budget direction over the next 12 months.

- Buying stage today.

- Largest marketing AI spend line.

Supporting metrics

- Budget Direction. Over the next 12 months your marketing AI budget will increase significantly, increase slightly, hold flat, or decrease. Reported as net direction, for comparability with the Gartner series, not as the lead.

- Buying Stage. Exploring, piloting, deployed in one channel or team, or scaling across the function. The go-to-market room's 21 of 25 is the seed of this series.

- Spend Allocation. Largest marketing AI spend line: martech tooling, internal build, agency and services, or data. Reported by category.

- Attribution Confidence. Confidence that current attribution would survive an outcome-priced contract, high, partial, or low. This is the question the consumption-pricing shift makes unavoidable.

Rotating deeper set (two or three per edition)

- Source of the marketing AI budget: net-new money, reallocated from agency spend, reallocated from planned headcount, or reallocated from other martech.

- Share of martech spend on consumption or usage pricing, in bands, for comparability with the Gartner consumption figures.

- Largest blocker to spending more: proving return, data readiness, talent, brand safety and governance, or integration.

- Expected time to measurable return, in months.

- Agents in production in marketing, yes or no, and in which loop: content, outreach, or full pipeline.

- Answer-engine exposure: whether the team actively optimizes for AI answer engines (GEO or AEO), a question our own room has already put on the table.

Collection

- Field the core at the next CMO Executive Forum gathering as Edition 1's first full collection, then add it to the registration flow for every CMO Executive Forum and CMO Dinner Series event.

- Ask only marketing leaders the budget questions, and report marketing-tagged so the operator read stays clean.

- Hold any headline figure until at least 40 marketing-leader responses sit behind it.

How It Runs

Sample and Honesty

The figures describe marketing leaders in the Open Future Forum community, a selective sample drawn from across multiple markets rather than a probability sample of all marketing organizations, and they are not presented as one. Every headline figure states its response base, no figure is published below 40 responses, and early editions are framed as directional reads of what operators in this community are doing. A smaller claim, fully backed, beats a larger one that invites the obvious critique.

Assets Each Edition Produces

- The published Report, for Substack and the site, written to be quoted and cited.

- A one-page summary graphic led by the CMO AI Leverage Index.

- A short methodology note, so the Report is citable as a source.

- A marketing-community cut, sent to the CMO Executive Forum list as its own short piece.

Distribution and Co-Branding

The Report is a natural co-brand for a martech, agency, or capital institution already in the Open Future Forum network, since the CMO read is the lane flagship. A sponsor receives logo placement and a data appendix. The independence terms below are not negotiable and run in the same edition, so the sponsorship never touches the numbers. Running Edition 1 fully independent, before any logo appears, is the cleaner way to set the tone.

- “The CMO AI Leverage Report reads how marketing leaders in the Open Future Forum community are funding and getting leverage from AI.”

- “In the Open Future Forum go-to-market room, 21 of the 25 registrants who answered the stage question are past exploration with AI agents.”

- Once the instrument clears the response floor, always cite with the response base: “Among the marketing leaders in this edition (n = X), Y percent say AI now lets them do more without adding headcount or agency spend.”

Suggested Citation and Versioning

Cite as: Open Future Forum, The CMO AI Leverage Report, Edition 1, July 2026.

The Report is a recurring series, released as the data supports rather than on a fixed schedule. Each edition carries a lane, an edition number, and a date, lives at a stable URL, and supersedes nothing. Prior editions stay published so the Leverage Index line can be tracked. Short handle for repeat reference: the CMO AI Leverage Index.

Methodology and Disclosure

Methodology Note

The CMO AI Leverage Report is produced by Open Future Forum. Demand-context figures are drawn from registration records for Open Future Forum events and describe registrant demand and composition; they are reported as distinct-registrant floors and may include individuals who register for more than one event. Index and supporting figures are drawn from a direct instrument fielded to event registrants who are marketing leaders, reported marketing-tagged with the response base stated and a minimum base of 40 per published figure. The early reads shown in this edition sit below that floor and are labeled as directional. Two limits apply to them and are stated plainly. First, the instrument questions were added partway through registration at both the CMO mixer and the go-to-market event, so only later cohorts answered them, which is why those bases are 7 and 16. Second, the rooms were role-mixed, drawing marketing operators alongside founders, engineers, and communications leaders, so the reads describe who was in those rooms, not a clean panel of CMOs. We report them anyway, with the base on the face of each figure, because the direction is informative and because showing the work is the point. External benchmarks from Gartner, MIT, Menlo Ventures, and BCG are attributed and used only for context. Open Future Forum runs the events and sells sponsorships; sponsorship does not influence the questions, the analysis, or the findings, and the Report does not rank or recommend vendors.

Independence and Disclosure

- Open Future Forum runs the events and sells sponsorships, and Murray Newlands does fractional advisory work with AI companies.

- Sponsors receive logo placement and a data appendix. Sponsors do not see, shape, or approve the questions, the analysis, or the findings.

- The Report never ranks, scores, or recommends specific vendors or products. It reports aggregate behavior only.

- Any company connected to Open Future Forum or Murray Newlands that appears in the Report is disclosed as such.

- The findings are the community aggregate. The Report is not a lead-generation instrument and does not pass respondent contact data to sponsors.

This statement runs in every edition.

About Our Events

Open Future Forum convenes marketing and growth leaders through the CMO Executive Forum and the CMO Dinner Series, a program of small, off-the-record dinners and gatherings for C-suite executives, held alongside its finance, security, and founder programs. Partner institutions support the events. They do not endorse or contribute to this report, which is editorially independent.

About Open Future Forum

Open Future Forum is a private executive community in Silicon Valley that runs small, off-the-record dinners for C-suite executives, with over 100 events since 2019 bringing together senior executives, founders, and investors. It runs the CMO Executive Forum, the CFO Executive Forum, the CISO Executive Forum, and related peer groups, including the CMO Dinner Series. The CMO AI Leverage Report is part of its operator-level research program.

Sources

Third-party figures cited in this report are drawn from the sources below. External benchmarks are used for context only. They are not affiliated with this report and do not endorse it.

- Gartner. 2026 CMO Spend Survey (401 CMOs and marketing leaders, North America, UK, and Europe, fielded January to March 2026). AI budget share, readiness, budget levels, labor share, martech share, and consumption pricing. gartner.com

- Gartner. 2026 CMO Spend Survey media findings. Media spend distribution and AI channel shifts. gartner.com

- MIT NANDA. The GenAI Divide: State of AI in Business 2025 (July 2025). The functional distribution of enterprise AI budgets, including the sales and marketing share, and pilot outcomes. nanda.media.mit.edu

- Menlo Ventures. 2025: The State of Generative AI in the Enterprise. Departmental and category AI spend. menlovc.com

- Boston Consulting Group. BCG AI Radar 2026: As AI Investments Surge, CEOs Take the Lead. CEO AI decision-making. bcg.com

- McKinsey & Company. Research on enterprise AI adoption and value capture by industry. mckinsey.com

- Deloitte. Enterprise AI adoption by industry. deloitte.com

- NVIDIA. State of AI 2026. Industry adoption and return. nvidia.com

- Chief Marketer. Reporting on the 2026 Gartner CMO Spend Survey, including martech share and consumption-pricing detail. chiefmarketer.com

- Marketing Dive. Reporting on the 2026 Gartner CMO Spend Survey and media spend findings. marketingdive.com

External benchmarks are used for context only. They are not affiliated with this report and do not endorse it.

This report is published by Open Future Forum for general information and research purposes only. It is not legal, financial, investment, tax, accounting, or other professional advice, and it should not be relied on as such. Nothing in it is a recommendation to buy, sell, or hold any security, product, or service, or to adopt any particular budget, vendor, or course of action. Figures drawn from Open Future Forum events are early, directional reads on small and self-selected samples, and figures from third parties belong to the organizations cited and are used for context. Readers should do their own research and consult their own qualified advisors before making decisions. Open Future Forum makes no warranty as to the accuracy or completeness of the information in this report and accepts no liability for any action taken in reliance on it.

© 2026 Open Future Forum. All rights reserved. The CMO AI Leverage Report and the CMO AI Leverage Index are works of Open Future Forum. No part of this report may be reproduced or redistributed for commercial purposes without permission. Quotation for journalism, research, and commentary is welcome with attribution to Open Future Forum. All third-party names and marks belong to their respective owners.

Join the CMO Dinner Series

Private invitation-screened dinners for marketing and growth leaders navigating AI budget decisions, agency strategy, and headcount leverage. Off the record. No vendors. No agenda.