Executive Summary

This is a preview edition, and it says so on purpose. The instrument behind the Executive AI Leverage Report went live across the Open Future Forum rooms in mid-2026; what follows are its first reads, most of them directional, published now because the direction is already worth having. Edition 1 ships when the flagship reading clears this program's response floor. Until then, these figures stand as the baseline the series will be measured against, and every one carries its base on its face, which is where we put it.

The preview reads executive AI leverage in two layers, in this order. First the data: instrument questions answered through applications to seven Open Future Forum events in 2026, spanning finance, security, growth, and founder rooms, with every figure carrying its base. Then the practice: Open Future Forum peer-learning sessions where finance leaders compare live deployments, read closely as the qualitative layer that shows what the numbers look like in an operator's hands.

The data says six things. The network is already deployed, not exploring: 71 percent of the largest finance room runs an AI tool today, and 14 of 16 in the growth room are past exploration with agents. The gate on the next dollar is proof, inside a short window: proving ROI is the top blocker at 53 percent, and 62 percent expect measurable return in under 6 months. The leverage thesis has its first budget-level measurement: one in six finance-room respondents already funds AI from money that would have been headcount. Authority and accountability sit in different seats: the CEO is the most named signer at 47 percent, finance second at 26. Security names the problem, securing AI agents at 56 percent, but only 31 percent have a budget line for it. And the supply side has moved off seat pricing: half of charging founders price on usage and 18 percent on outcomes, while founders sell to the CIO and the business unit, barely seeing finance at all. That last mismatch, the seat gap, is the edition's sharpest cross-lane finding, and a first vertical cut of the founder data shows the doors differ by industry: the CIO owns enterprise software, the business line owns fintech, and healthcare is the slowest to monetize.

The rooms then explain the how. Their practitioners describe leverage arriving in three stages, and can say which one they are on: productivity, AI as a thought partner; capability, AI as a co-worker doing whole units of work; and context, AI that knows the business well enough to ask the right questions itself, visible but not yet reached. We formalize that as the Executive AI Leverage Ladder, and the rooms' practices — compression, cost discipline, process blueprinting, governance, revenue-side use — map one to one onto the data findings: they are how operators prove return inside the six-month window, pass the ROI gate, and live inside the headcount mandate the surveys detect.

Open Future Forum, 2026. Surveys: 421 responses across seven events, bases stated per figure. Sessions: Open Future Forum finance peer-learning events, 2026, qualitative.

What This Report Reads, and How It Differs from the Budget Work

Open Future Forum runs two kinds of operator research from the same rooms. The Enterprise AI Buying & Budget Index, whose first edition is the CFO AI Leverage Report, reads the money: who signs, where the budget comes from, what blocks the next dollar. This report shares the framework, the honesty rules, and the community, and reads something else: the leverage itself. Part one below establishes, from the survey data, where executives stand and what gates them. Part two goes inside a room of operators to show what the leverage consists of when someone actually gets it, how it was built, what it cost in setup and discipline, and what broke along the way.

The findings in part one are quantitative, each with its base; bases below the program's 40-response floor are labeled directional. The practices in part two are qualitative and are reported as exactly that: small peer rooms, screened on purpose for being ahead of the curve.

Part One: What the Data Says

Six findings from instrument questions embedded in the application flow for seven Open Future Forum events in 2026; 421 applicants answered at least one instrument question. These are the series' baseline readings: the figures every later edition will be measured against. Because the questions sit in the application, the figures describe everyone who applied, not only those who attended. Several questions allowed multiple selections, so any-mention percentages can sum past 100; each chart states its base and conventions on its face. The rooms are role-mixed, drawing operators alongside founders, investors, and advisors, so these figures describe the rooms, not clean panels of the title on the door.

Data Finding 1: The Network Is Deployed, Not Exploring

At the largest Open Future Forum finance event of 2026, 71 percent of registrants said their team is already running Claude or another AI tool, 22 percent are evaluating, and 8 percent have not started, base of 185. That is a maturity profile, well past the exploration phase most 2026 coverage still assumes, and it sets the baseline for everything else in this report: the leverage question in this network is not whether to adopt but what adoption returns.

The growth lane reads even further along on agents specifically: 14 of 16 respondents at the agentic AI go-to-market event are past exploration, with 5 running agents in production across the business and 5 building agentic products, base of 16, directional. Agents in production means whole units of work already handed over, so the growth seat appears to be climbing fastest, which fits: marketing work tolerates iteration in ways month-close does not.

Data Finding 2: The Gate Is Proof, and the Window Is Six Months

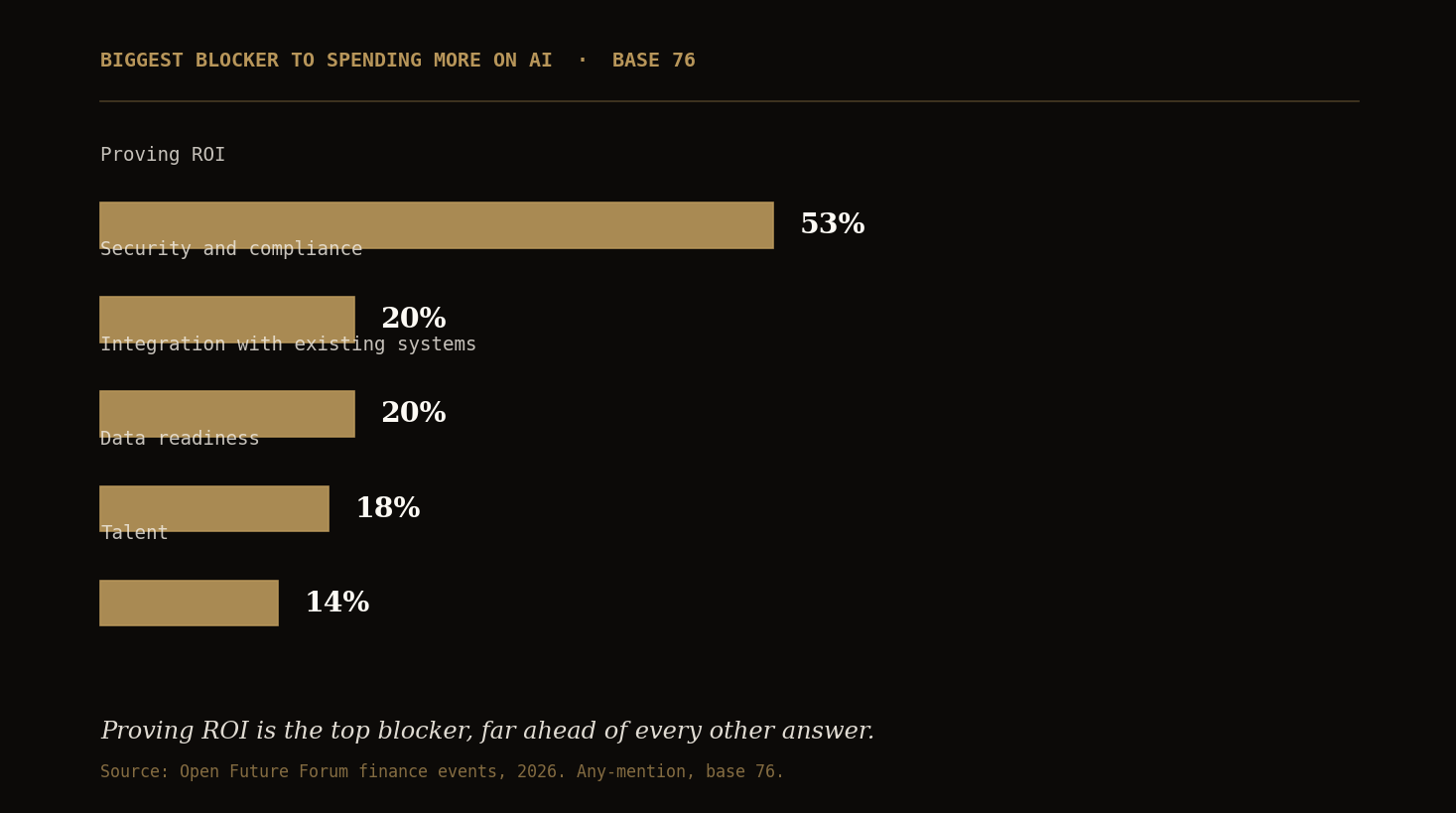

Asked the main thing stopping them spending more on AI, 53 percent of finance-room respondents named proving ROI, base of 76, far ahead of security and compliance at 20 percent, integration with existing systems at 20, data readiness at 18, and talent at 14. No other blocker came close, and the pattern held in both finance events independently. Read next to the macro, this is the reckoning arriving as a survey answer, and the macro is moving fast. MIT's The GenAI Divide: State of AI in Business 2025 found roughly 95 percent of enterprise generative AI pilots produced no measurable profit-and-loss impact, a figure widely quoted and fairly critiqued: it measured attributable P&L in a narrow window, and the same study found widespread unofficial AI use creating value nobody was counting. S&P Global Market Intelligence found the share of companies abandoning most of their AI initiatives jumped from 17 percent to 42 percent in a single year. Both readings point the same direction as this network's answer: the buyers are not abandoning AI, they are making measurement the gate.

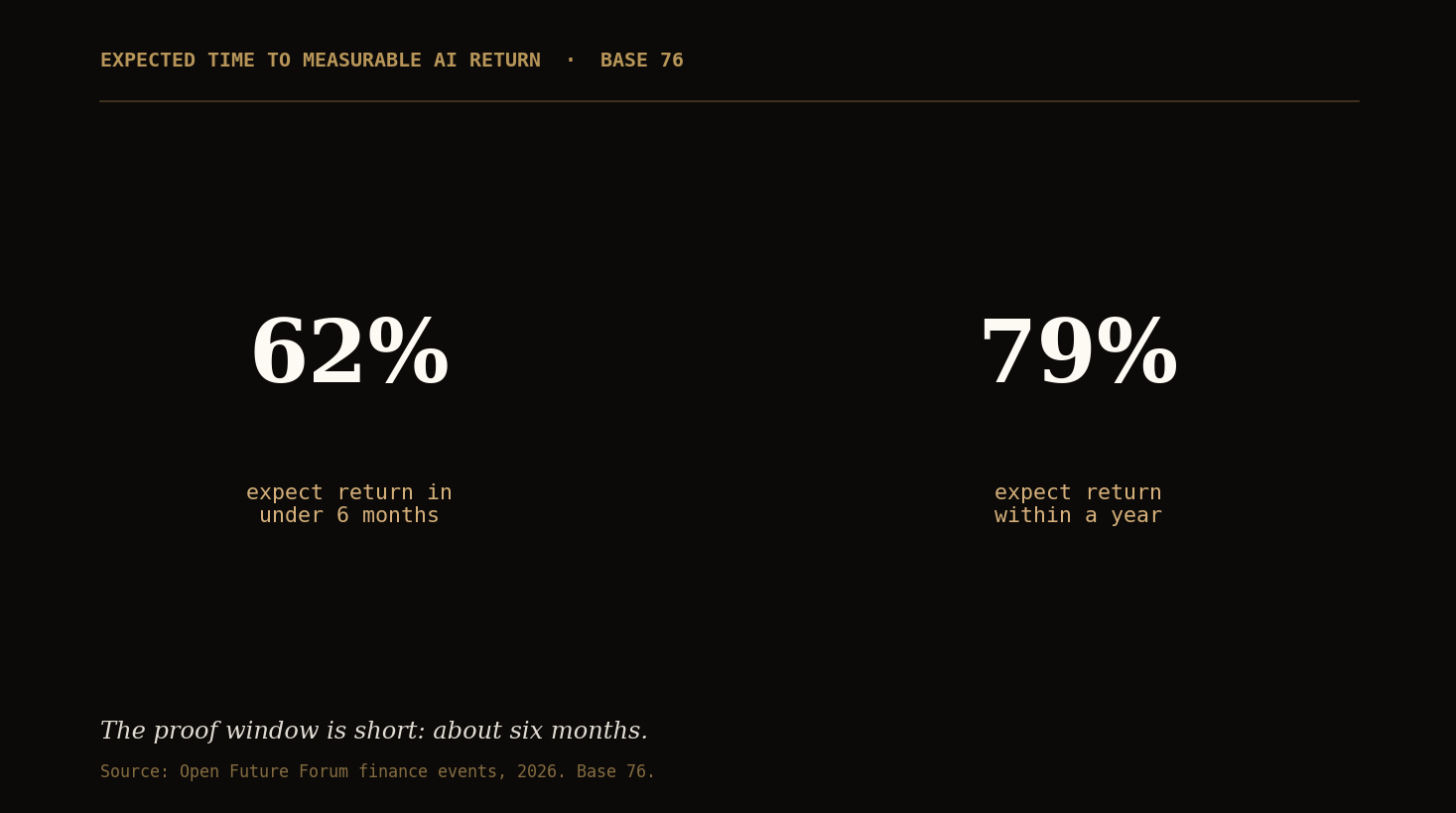

The window on that proof is short. 62 percent expect measurable return on an AI investment in under 6 months, and 79 percent within a year, base of 76. Two findings, one buying posture: the biggest blocker is proving ROI, and the window to prove it is about six months. Anyone selling into this market on an 18-month value story is selling to a buyer who expects the proof in months.

Data Finding 3: One in Six Already Funds AI from Would-Be Headcount Money

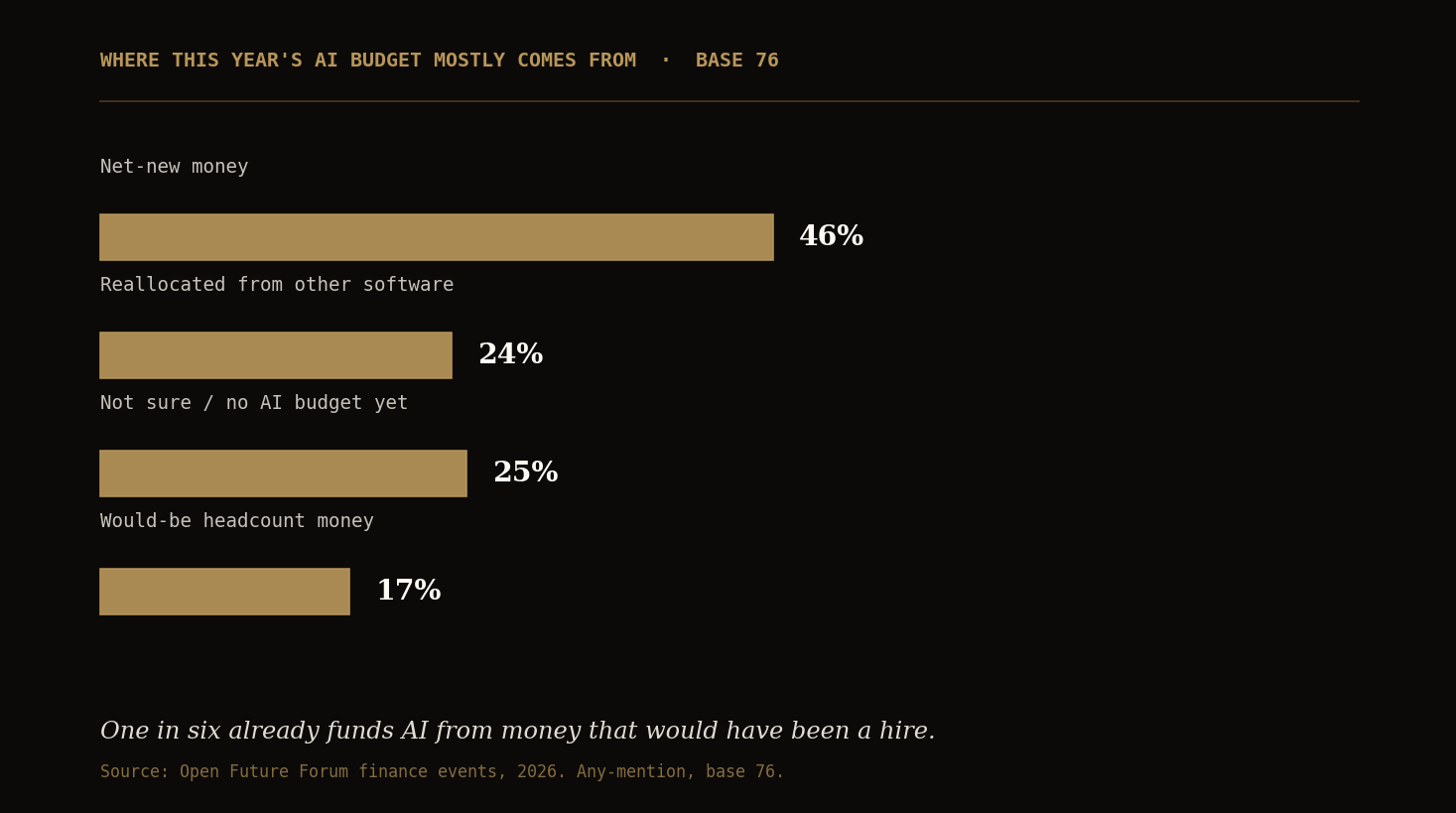

Asked where this year's AI budget mostly comes from, 46 percent of finance-room respondents said net-new money, 24 percent said reallocated from other software, and 17 percent, roughly one in six, said money they would otherwise have spent on headcount, base of 76, any-mention; 25 percent said not sure or no AI budget yet. The 17 percent is the first direct, budget-level measurement of headcount leverage in this network: the hire not made, funding the tool that replaces the hire. The fuller picture keeps it honest: with net-new still dominant, leverage today is being bought more than it is being harvested. The one-in-six is the leading edge, and whether it grows is the line this report will track.

Data Finding 4: The CEO Signs, Finance Answers

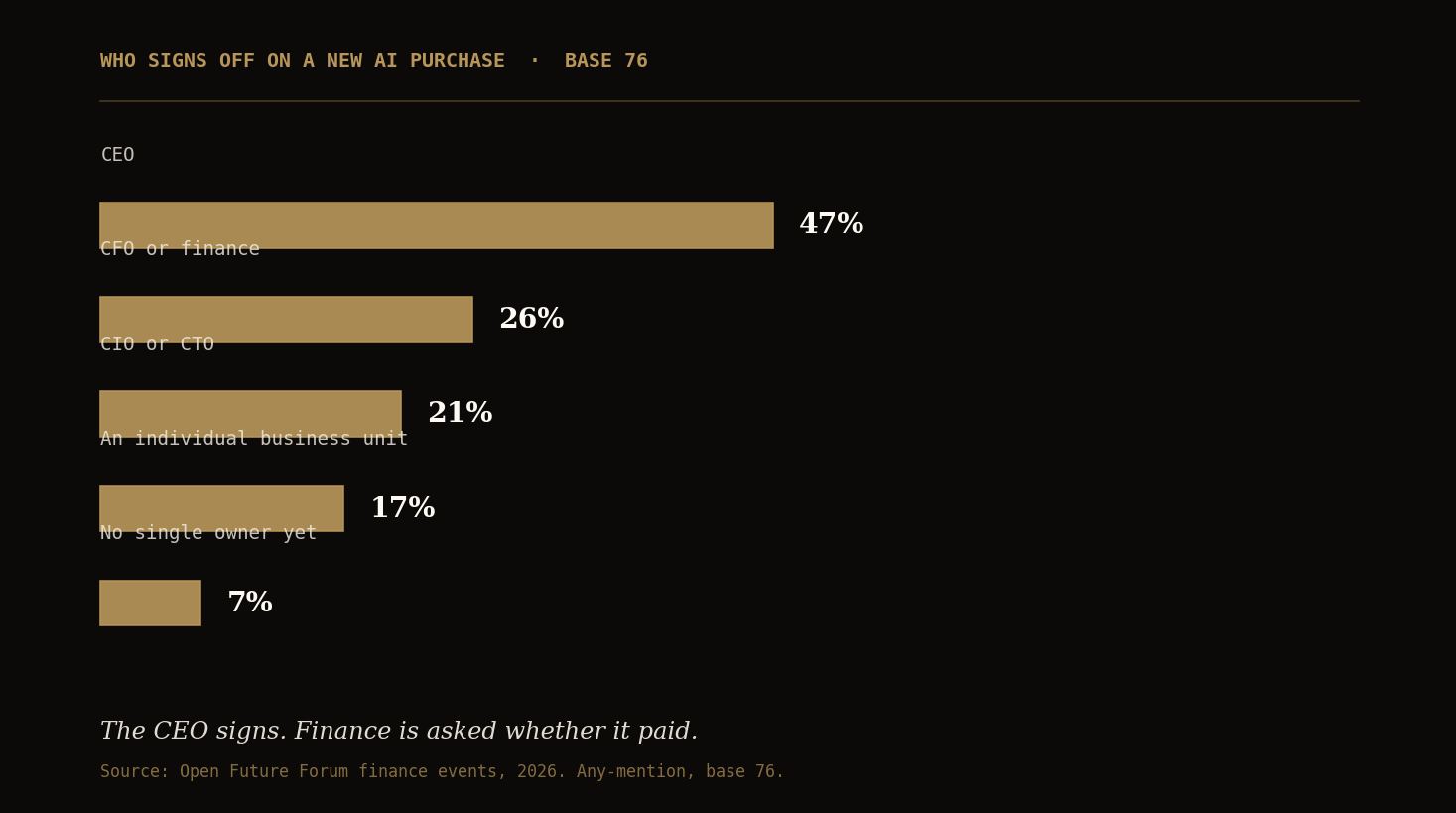

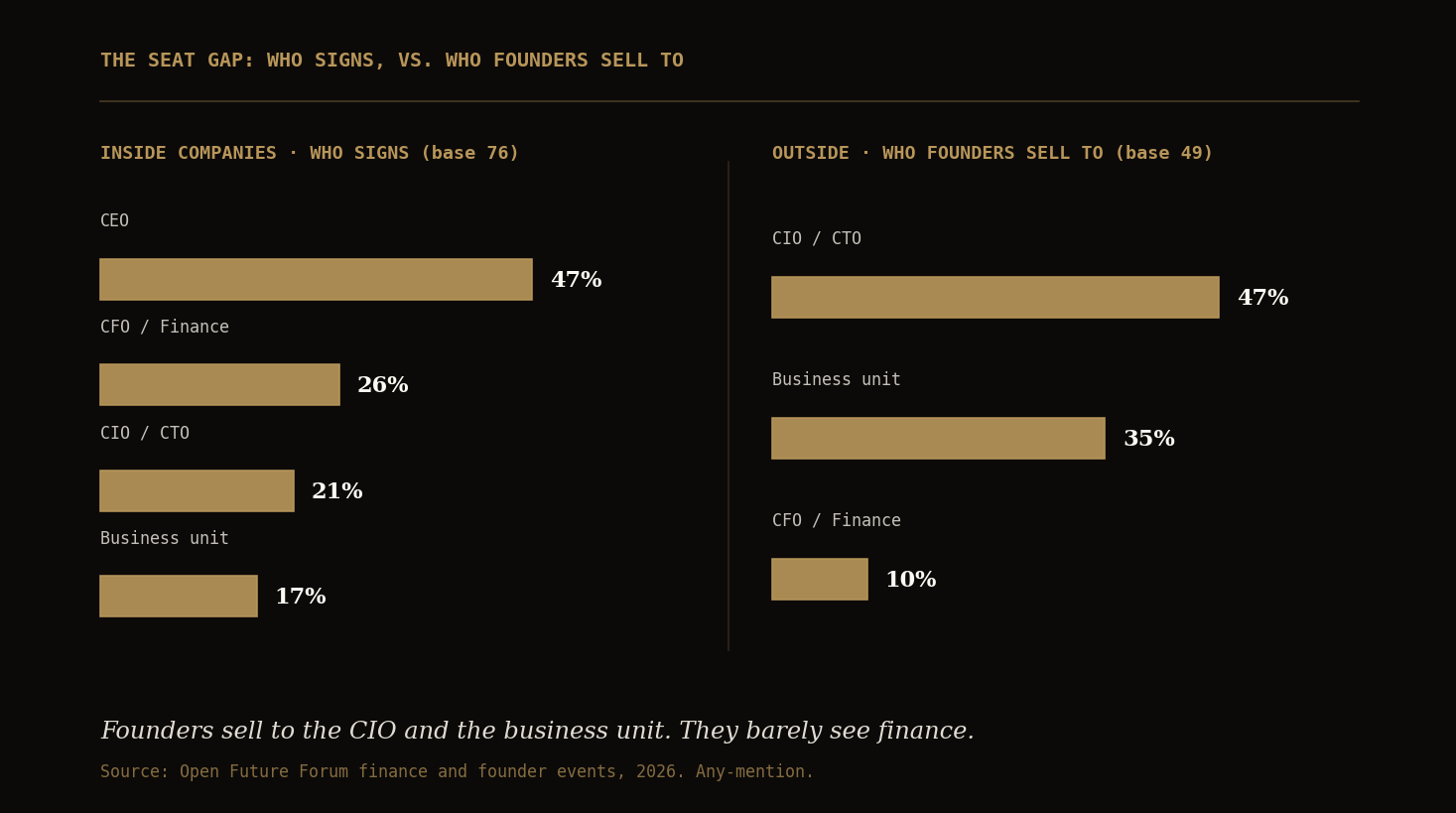

Asked who signs off on a new AI purchase, 47 percent named the CEO, 26 percent the CFO or finance, 21 percent the CIO or CTO, 17 percent an individual business unit, and 7 percent said no single owner yet, base of 76, any-mention. This lines up with BCG's AI Radar 2026, a survey of 2,360 executives, which found 72 percent of CEOs calling themselves the main AI decision-maker. Put next to data finding 2, it defines the governance shape of the market: the seat that signs is not the seat that proves. The CEO holds the pen; the function, most often finance, is asked whether it paid. That gap between authority and accountability is where the leverage practices in part two live, and this figure is the series' reference read on AI buying authority: the one later editions test first.

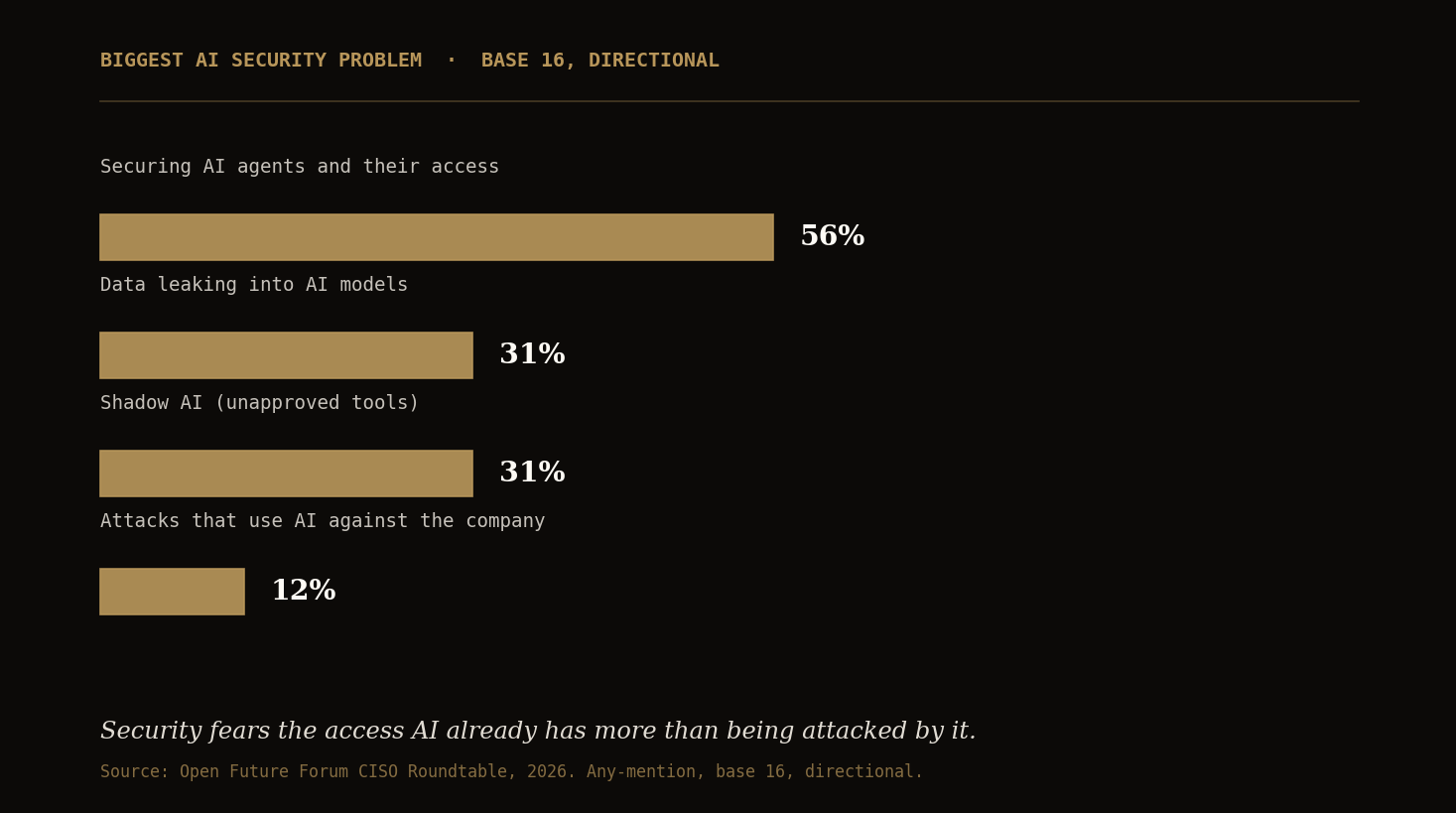

Data Finding 5: Security Names the Problem but Lacks the Line

Asked the biggest AI security problem on their desk, 56 percent of security-room respondents named securing AI agents and their access, with data leaking into AI models and shadow AI (tools the organization uses without approval) each named by 31 percent; attacks that use AI against the company came last at 12 percent, base of 16, directional. The seat responsible for security is worried less about being attacked by AI than about the access the AI already deployed inside the company has.

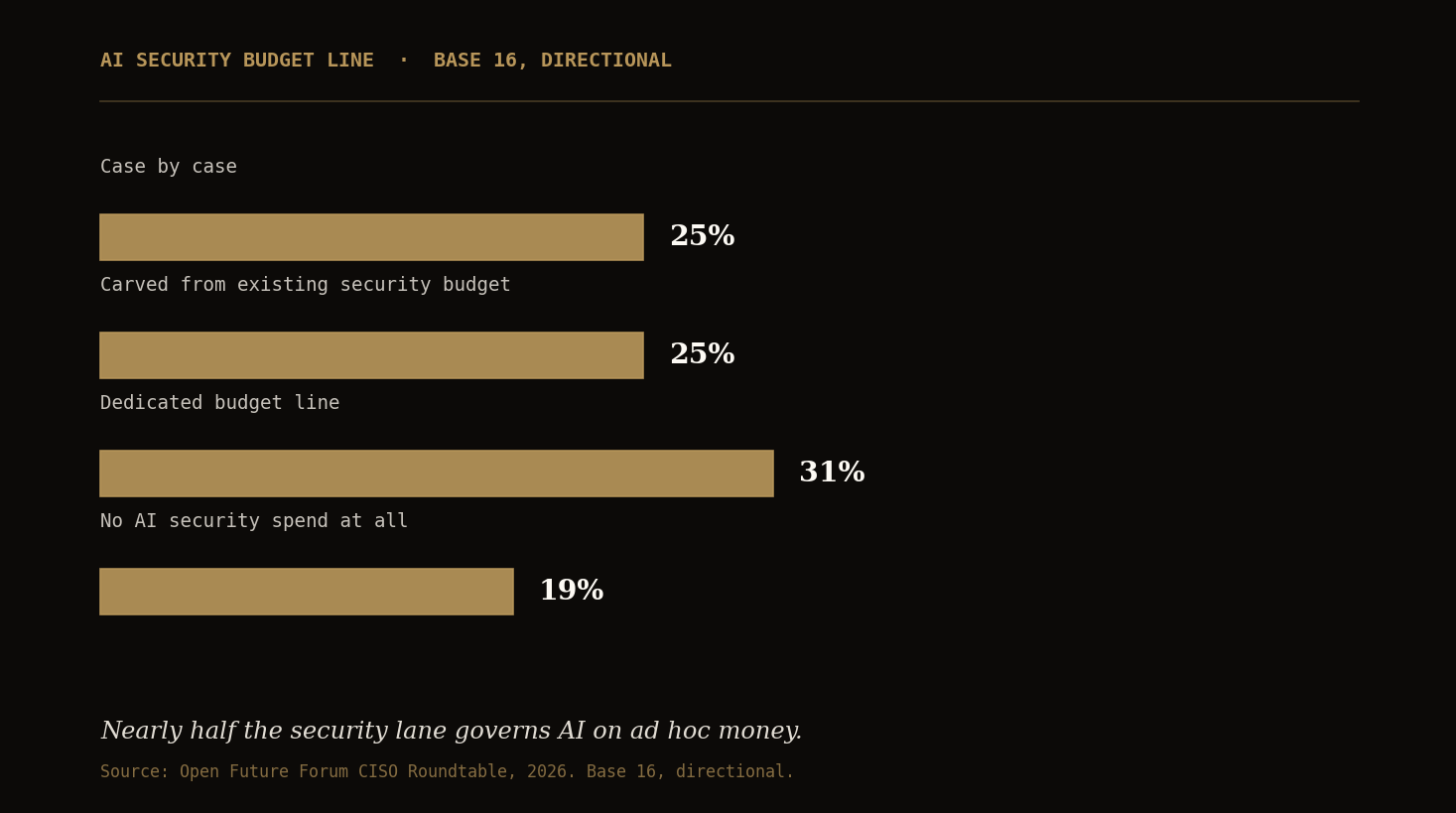

The funding lags the worry. Only 31 percent said AI security has its own budget line; 25 percent carve it out of the existing security budget, 25 percent fund it case by case, and 19 percent have no AI security spend at all. Nearly half the security lane is governing production-grade AI on ad hoc money. Read against the MarketsandMarkets forecast of the agentic AI security market growing from about $1.65 billion to $13.5 billion by 2032, the gap between the named problem and the dedicated funding is the budget motion still to come.

Data Finding 6: The Supply Side Has Left Seat Pricing Behind

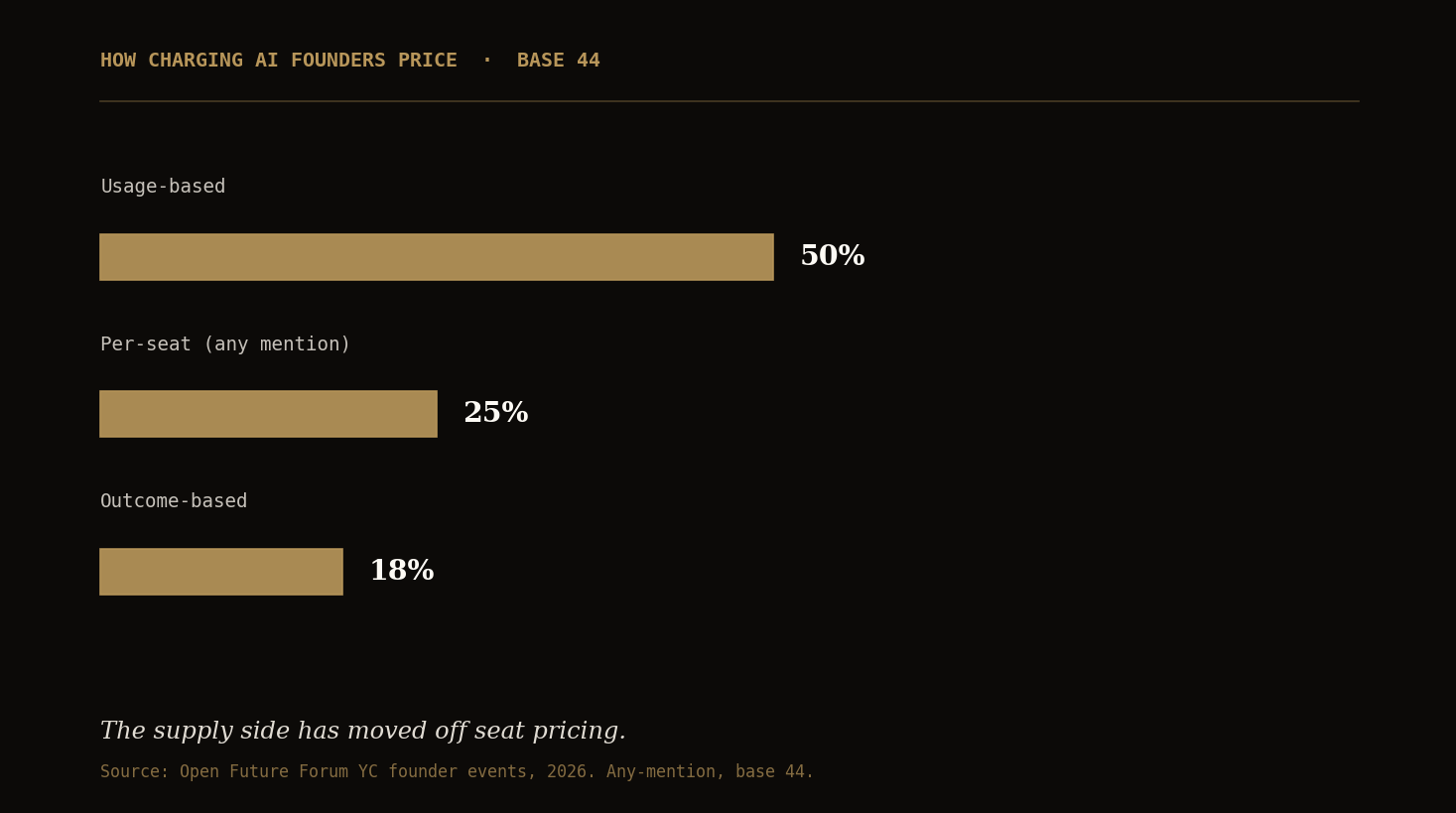

Across the founder cohort in the network, half of those charging price on usage and 18 percent on outcomes, paid when it works, against 25 percent who mention per-seat at all, base of 44, any-mention. Asked who owns the buying decision inside the companies they sell to, 47 percent named the CIO or CTO, 35 percent a business-unit leader, and 10 percent the CFO or finance, base of 49, small but no longer zero in this network's reads. Usage pricing charges for what the buyer consumes; outcome pricing charges for what the buyer achieves. Both are auditable in a way seat licenses never were, and auditable pricing is built for the buyer the proof gate in data finding 2 is training executives to be. The metering has arrived ahead of the purchasing authority it implies.

Leverage by Seat: The Data Read per C-Level

A report called executive owes each executive their own read, so before moving inside the rooms, here is what the six data findings say seat by seat: where each C-level's budget authority sits and where it stands. Each seat carries its own data card; because a card draws on more than one question, the base is stated on every bar, and gold marks an external benchmark. Security and growth reads are directional.

The CEO: Holds the Pen

The most named signer of a new AI purchase at 47 percent, base of 76, consistent with BCG AI Radar 2026's 72 percent. The read: the CEO owns the decision but not the practice. Nothing in the craft that part two describes, the caps, the routing, the blueprinting, lives in the CEO's office, which means the seat with the pen is the seat furthest from the leverage. The executives who close that gap for their CEO are the ones whose budgets extend.

The CFO: Holds the Accountability

Named as signer by 26 percent, but carrying the fullest data profile of any seat: 71 percent of the finance room already running an AI tool, 17 percent already funding AI from would-be headcount money, the proof gate at 53 percent, and the six-month expectation at 62 percent. The read: finance is the seat where the leverage thesis is furthest along and most explicitly demanded, and the seat every other row of this section eventually reports to on return.

The CIO or CTO: The Door the Market Knocks On

Named as internal signer by 21 percent, base of 76, but named as the buyer by 47 percent of the founders selling in, base of 49. The read: the technology seat is the default entry point for outside AI even where it no longer holds the decision inside. That mismatch, drawn in the chart below, is where vendor sprawl originates: what enters through the CIO's door gets answered for at the CFO's desk.

The CISO: Funds the Counterweight

Top problem: the access AI itself has, 56 percent naming agent security, base of 16, directional. Budget: only 31 percent with a dedicated line. The read: governance is the price of everyone else's leverage, and it is currently the least-funded seat relative to its named problem. Expect this line to move toward dedicated funding, and expect it to cross the CFO's desk as net-new.

The CMO and Growth Leader: Furthest Along on Agents

14 of 16 past exploration, 5 running agents in production, base of 16, directional. The read: marketing work tolerates iteration, so the growth seat adopts agents first and hits the measurement wall second, attribution being its version of finance's proof gate. The headcount-leverage question that defines the finance lane arrives here next.

The Business-Unit Leader: The Shadow Buyer

Named as internal signer by 17 percent and as the founders' target by 35 percent. The read: the business unit is the second door into the company and the first place shadow AI takes root, because it buys closest to the work and furthest from the inventory. The governance findings in part two are aimed squarely at this seat.

The Founder: Pricing Ahead of Its Buyer

Half of charging founders on usage, 18 percent on outcomes, one in ten naming finance as the buyer. The read: the supply side is building pricing a buyer can audit, by what is used and, increasingly, by what it returns. When that pricing meets the CFO's six-month proof window, the seat gap below closes from both sides.

The chart is the section's argument in one image. Inside companies, the CEO signs most and the CFO second; from the outside, founders aim at the CIO and the business unit, and barely see finance at all. Both readings are true at once, which is exactly how sprawl happens: AI enters through the seats that buy easily and is answered for by the seats that measure. Part two shows the practices that reconcile the two columns inside a company before the invoice does it for them.

Leverage by Vertical: Where the Industry Changes the Answer

Seats decide who buys and who answers for it; verticals decide how fast the answer comes. The founder applications include a self-described sector, which gives this report its first vertical read from first-party data: 76 founders classified by us into four verticals plus other, with multi-sector answers counted in each. The cells are small and reported as counts, directional throughout, and this is the supply side, the companies building and selling AI into each vertical. The buy-side texture underneath comes from the finance peer-learning sessions, whose participants span staffing, healthcare, insurance, investment firms, SaaS, and accounting.

Enterprise software and infrastructure dominates the founder mix, which is the supply side of data finding 1's deployment baseline: the deepest bench of builders is aimed at the most deployed buyers. The vertical reads below take the two questions that define this report's market, who buys and how it is priced, and split them by vertical. The pattern is not uniform, and the differences are the finding.

Enterprise Software and Infrastructure: The CIO's Vertical

Among founders selling enterprise software, infrastructure, and security, the buyer is overwhelmingly technical: 21 of 28 name the CIO or CTO, 10 the business unit, and just 2 name finance. This is the purest form of the seat gap: the biggest slice of the supply side sells almost entirely to the technology seat, while data finding 4 says the pen inside the buyer sits with the CEO and the accountability with finance. Pricing is mixed, 17 of 28 on usage or outcomes, with per-seat and flat subscription persisting here more than anywhere else.

Fintech and Financial Services: The Business Line Buys, and the Pricing Is Metered

Fintech inverts the enterprise pattern. The business-unit leader out-buys the CIO, 4 of 8 against 2, and usage-or-outcome pricing is near-universal: 7 of 8 charging founders. Where the product touches money directly, the buyer sits closest to the P&L and the pricing meters the value. This is the same industry the peer sessions know from the buy side, fund accounting reconciliations redesigned around agents, insurance and investment operators in those sessions, and it matches the external picture of financial services as among the most-adopted and best-proven AI industries (Deloitte enterprise adoption surveys; NVIDIA, State of AI 2026).

Healthcare and Life Sciences: The Slowest to Monetize

Healthcare founders show the most scattered buyer, 3 CIO, 3 business unit, 2 finance of 10, and the weakest monetization: 2 of 10 are not charging at all, the only vertical where that answer appears, and only 5 of 10 price on usage or outcomes. This is what a compliance-gated vertical looks like from the supply side: the sales motion is slower, the buyer is less standardized, and revenue arrives later. It mirrors the external adoption curve, healthcare climbing fast but from behind, and the buy-side version in our sessions, where healthcare finance operators were among the most governance-focused at the table.

Consumer: Usage-Metered by Default

The smallest cell, 5 charging founders, but the cleanest pricing signal: 4 of 5 on usage. Consumer AI meters like a utility because its value is consumed per interaction. The buy-side echo from the sessions is the demand-forecasting story, consumer-goods forecasting once measured in consulting months, re-scoped to days, the vertical where AI touches revenue more directly than cost.

The External Picture, for Context

The industry adoption curve underneath these supply-side reads, drawn from external benchmarks and attributed as such: technology and software lead at roughly 92 percent adoption, and financial services sits close behind in the high eighties (Deloitte; NVIDIA, State of AI 2026). Healthcare and life sciences are accelerating to about two thirds, and manufacturing sits around half to two thirds with the cleanest cost-out case (representative of McKinsey and Deloitte 2026 cross-industry surveys). Retail and consumer firms are among the highest adopters of agentic AI specifically (2026 cross-industry surveys). Adoption rates vary widely by source, definition, and survey year, more than any other figure family in this report, so treat this as directional: the ordering of industries is stable across sources even where the levels are not. As the founder sector base grows, this program will replace this external panel with first-party vertical readings.

Read together, the vertical layer says what Edition 1 of the budget work said from the buy side: where the return is measurable, the vertical moves fast and prices for outcomes; where it is gated, by compliance in healthcare, by integration in the enterprise stack, the vertical is slower and the pricing stays conventional. The industry does not change the leverage question. It changes how quickly the answer comes, and through which door.

Part Two: Inside the Rooms

The data establishes where the network stands: deployed, gated on proof, expected to show return inside six months, with authority and accountability in different seats. What the data cannot show is what passing that gate actually looks like. For that, Open Future Forum convenes finance leaders in peer-learning sessions, screened so that nearly all are already running Claude or another AI tool in their work, drawn from staffing, healthcare, insurance, investment firms, SaaS, and accounting, where operators compare live deployments in their own words. This part is the structured read of those rooms: one framework and seven practices, each mapped back to the data finding it explains. It is qualitative and reported as exactly that.

The Executive AI Leverage Ladder

The framework this report leads part two with came out of the rooms, not out of a slide. In session, one operator summarized the year plainly: the function has migrated from productivity to capability, and the next stage is AI that provides the context and asks the right questions itself. The rest of that room recognized the description immediately, and once you have it, every story told in these sessions, and every figure in part one, sorts onto one of three rungs.

Rung one, productivity: AI as a thought partner. Knowledge inquiry, drafting, learning something new before doing it the old way. Finance leaders described exactly this posture as deliberate policy, unlimited AI for learning and low-risk checks, with forecasting and sensitive data explicitly kept out. Real value, but the work still flows through the human at the same width it always did.

Rung two, capability: AI as a co-worker. The stage the rooms now occupy, and the one that changes the math. The operators' language has shifted from asking AI things to instructing it: session decks are built by Claude on instruction, not by hand. AI does whole units of work, builds the three-statement model, runs the monthly reconciliation on schedule, drafts the department budget sheets and rolls them back up. Repeatable instructions get captured as skills, a recipe book of steps and guardrails, so the capability compounds; agents get shared across teams, single analysis agents serving entire strategic finance organizations. This is where headcount and output decouple. The 17 percent headcount-money figure in part one is the budget trace of this rung, and the 71 percent deployment figure is the population climbing toward it.

Rung three, context: AI that asks the right questions. Visible, not reached. Today the executives know which questions to ask, and they are explicit that this is their remaining edge. Rung three is when the system knows the business well enough to surface the question itself. Several participants put a timeline on it of roughly a year; whether they are right is exactly what this report will track.

Practice 1: Compression, or How the Six-Month Window Gets Met

Data finding 2 says 62 percent of the network expects measurable return inside 6 months. The rooms show how that window gets met, and they did not talk in percentages; they talked in before-and-after durations. A three-statement corporate model, built natively in Excel: three to five days before, a couple of hours to a working baseline now. A full driver-based planning model with department roll-ups: built inside a working day. Audit-season subledger-to-general-ledger reconciliation: uploaded, and returned as a work paper with the journal entry and the explanation. Demand-forecasting engagements that once took consulting teams months, re-scoped by the practitioners who ran them to collaborations measured in days. A weekly FX-rate refresh that was a manual Friday routine, now a scheduled script written entirely by prompting, by an operator who wrote no code by hand.

Compression is the honest unit of executive leverage because it is observable and hard to inflate. Adoption percentages flatter; hours do not. Days-to-hours compression is how an operator proves return inside six months, which is why the instrument at the end of this report asks for compression directly.

Practice 2: The Headcount Mandate, or the 17 Percent in Person

Data finding 3 found one in six funding AI from money that would have been headcount. The rooms supplied the same figure as an employment condition. Finance leaders in the sessions described mandates set in exactly these terms: the team stays at its current size, the team will not grow, and Claude is expected to carry a growing share of the work. That is the leverage thesis converted from a budget line into a job description, and it is what Gartner's macro line, finance headcount-growth expectations falling from 6 percent to 2 percent, looks like from inside.

The external record is moving on this faster than any other finding, in both directions. Stanford Digital Economy Lab research in 2025 found early-career workers in the most AI-exposed occupations experiencing a roughly 13 percent relative decline in employment, the entry-level version of the mandate. And Klarna is the caution running the other way: after saying in 2024 that its AI assistant did the work of roughly 700 agents, its CEO said in 2025 the cost-cutting had gone too far on quality and reintroduced human service options. Adopted, overshot, rebalanced. Worth stating with equal weight: nobody in the sessions described layoffs. The mandate arrives as teams held flat while scope grows, which is precisely the do-more-without-adding-headcount formulation, and it is why the affected operators were in the rooms learning the other six practices.

Practice 3: Cost Discipline, or How the Proof Gate Gets Passed

Data finding 2 says proving ROI gates the next dollar. The rooms' second-loudest theme was the practice that passes the gate: managing the unit cost so the return is defensible. Operators at large organizations described monthly AI allowances that now run out well before month end. The response pattern among the further-along companies was consistent: set usage limits across the company first, the way you would set limits on a company card, then find out who is using it for what and extend where the value is proven. Then notice that every model defaults you to its most expensive setting, and dial routine work down. One company described routing common internal questions to cheaper models and caching repeated answers, with claimed savings of roughly half of AI cost. At the far end, high-volume teams run private model deployments inside their own cloud tenancy for sensitive, repetitive work.

Cost discipline is not the opposite of leverage; it is a leverage practice. And per data finding 4, it is also how an operating executive earns standing with the seat that signs: the CEO holds the pen at 47 percent, so the operator who can show cost per outcome is the one whose requests get extended.

Practice 4: Process Blueprinting, or What the Integration Blocker Really Is

After proving ROI, the most named blockers in data finding 2 are integration with existing systems at 20 percent and data readiness at 18, and the rooms' veterans explained what those answers actually mean: they are process problems wearing technology clothes. Asked where transformations fail, the rooms were unanimous, and it was not the model. Transformations fail at the process level: undocumented business logic, unclear data lineage, capital-allocation rules that exist only in someone's head. The phrase that carried the evening was process blueprinting: who does what, how, and with which data, documented well enough that an AI co-worker can take it over, and reimagined rather than merely transcribed, because agents make whole steps of the old map unnecessary. One worked example: a fund-accounting reconciliation where humans once looked up every discrepancy across data platforms by hand, redesigned so the agent does the lookups and the human adjudicates the exceptions.

The rooms also flagged what is coming for this bottleneck: software that watches how work actually flows across an organization's machines and derives the process map automatically. Several startups are building exactly that, and the practitioners' verdict was that process blueprinting is where the consulting opportunity, and the consulting disruption, both live.

Practice 5: Governance, or the CISO Data Lived

Data finding 5 found the security lane naming AI agent access as its top problem while mostly lacking a budget line for it. The rooms supplied the lived version. The sharpest pattern: companies whose audits of live AI data connections found several times more than their IT leadership had estimated. Shadow AI, employees running company or client work through personal AI accounts, came up repeatedly as the risk nobody can currently chase, exactly the 31 percent shadow-AI answer in the security survey. The rooms' rule of thumb was blunt: the confidentiality risk inside the company may exceed the risk outside it, because internal data flows are the ones nobody is watching. And a finance-specific discipline surfaced alongside: for work that must be exactly right, use AI to build the automation, then run the automation deterministically, rather than asking a model to re-execute the task fresh each time.

The demand signal was unambiguous. Participants asked, unprompted, for introductions to firms doing AI validation and data-governance workflow design, and offered each other integration help on the spot. Where operators request categories by name while the security lane still funds case by case, budgets follow.

Practice 6: Revenue Leverage, or Where Outcome Pricing Points

Data finding 6 shows the supply side charging by usage and, in a smaller but growing share, by outcomes. Outcome pricing only functions where value can be measured at the transaction, which is revenue and cash-flow territory, and the rooms' most forward-leaning operators are already working that territory from the buy side. The practices described: analyzing contracts for payment terms to pull cash flow forward; reviewing sales contracts for risk fast enough to speed deals up rather than slow them down; deep-researching counterparties, their vendors and connections, before revenue is booked; and reading which salespeople bring which quality of contract. CFOs in the network describe the shift from cost-cutting to revenue and cash-flow work as the real change in how the company sees the finance function. A second-order point from the same discussion: AI-risk language in contracts, what a customer may do with your data, has itself started slowing enterprise sales, which puts contract review about AI on the same desk as contract review by AI.

Practice 7: Expertise, the Multiplier with a Half-Life

The rooms' answer to the replacement question was neither denial nor despair. It was a claim about compounding: AI is an amplifier for people with deep domain knowledge, because the output is only as good as the questions asked and the judgment applied to what comes back. The rooms' veterans called it context, the dirt-under-the-fingernails knowledge of how the business actually works, earned cross-functionally, and they were explicit that it is the current edge and the thing to teach the next generation. They were equally explicit that the edge is temporary, which is rung three of the ladder: the moment the system can supply the context and ask the questions, the multiplier moves again. The honest version of this practice is therefore a pair: expertise is the multiplier today, and the half-life of that multiplier is the open question this report will track.

What the Rooms Say Is Coming

Peer rooms of operators are also an early-warning system, and four forward claims recurred with enough conviction to record. They are predictions made in the rooms, reported as such, not findings.

- Accounting is next after coding. Participants relayed frontier-lab engineers describing coding as largely solved, and the rooms' read was that structured, rule-governed finance work sits next in line. The practitioners saying this were not alarmed; they were repositioning toward judgment, context, and process design.

- Forward-deployed engineers are coming for the software stack. AI companies raising large rounds are moving into implementation: going into enterprises, replacing incumbent software with AI-built workflows directly. The rooms treated this as the successor to the consulting model.

- AI-native private equity is the extreme case of the leverage thesis. Funds are being raised to buy companies in chosen verticals and rebuild them AI-first, top to bottom, the whole-portfolio version of doing more without headcount. The rooms debated the economics and the humanity of it in the same breath, which is the honest state of the question.

- Non-technical teams will ship products. The example cited: a marketing team at a mid-sized enterprise company that built and launched a consumer-grade product with no developers engaged. The open question posed to the rooms, still unanswered: which CFO produces the first new business model the same way.

The Moving Market: Change Is a Finding Here

This report covers a market moving faster than the benchmarks describing it, which this program treats as an asset rather than a hazard. Every edition re-reads its external benchmarks and its own baseline readings, and reports what moved, in the open. A changed number is a finding here, not an embarrassment. Three movements already sit under this preview.

- The abandonment rate more than doubled. S&P Global Market Intelligence found the share of companies abandoning most of their AI initiatives rose from 17 percent to 42 percent in a year. Read with this network's data, that is the proof gate closing on unmeasured deployments, and it makes the cost-discipline and compression practices in part two more valuable, not less.

- The headline failure statistic is already being re-litigated. MIT's 95 percent no-profit finding dominated the 2025 discourse, and its critiques, that it measured narrow P&L attribution and undercounted unofficial use, are now part of the record. This program's position: the statistic and its critique support the same conclusion, that value exists where measurement does not, which is exactly the gap the instrument measures.

- The headcount story has already reversed once. Klarna went from AI doing the work of roughly 700 agents to reintroducing human service inside two years. The leverage thesis is not a straight line, and this program will report reversals in its own numbers with the same prominence as advances. The 17 percent headcount-money figure is the line to watch in both directions.

The commitment this section makes is standing: where an external benchmark this report cites is revised, disputed, or superseded, the next edition says so at the figure. Where this program's own numbers move as bases grow, as the sign-off reading did between the budget work's early read and its full base, the move is reported as a finding. In a market like this one, the record of what changed is worth as much as any single reading.

Each prediction has a data-finding shadow in part one: outcome pricing (finding 6) is the business model of the forward-deployed wave; the seat gap is the opening AI-native PE walks through; and the deployment baseline (finding 1) is what makes accounting-is-next plausible to the people who would know.

By the Numbers

The figures below are first-party reads from Open Future Forum rooms, each with its base. Survey figures come from instrument questions embedded in event registration; several allowed multiple selections, so any-mention percentages can sum past 100.

- 71 percent of the largest 2026 finance room already runs Claude or another AI tool; 8 percent have not started (base 185).

- 62 percent of finance-room respondents expect measurable return on an AI investment in under 6 months; 79 percent within a year (base 76).

- 53 percent name proving ROI as the main thing stopping them spending more on AI, the top blocker by a wide margin (base 76).

- 17 percent, roughly one in six, fund this year's AI budget at least partly from money that would have been spent on headcount (base 76).

- 47 percent name the CEO as the signer of a new AI purchase; 26 percent name the CFO or finance; 21 percent the CIO or CTO (base 76, any-mention).

- 20 and 18 percent name integration with existing systems and data readiness as their main blocker, the process problems behind the technology (base 76, any-mention).

- 56 percent of security-room respondents name securing AI agents and their access as the top AI security problem; only 31 percent have a dedicated AI security budget line (base 16, directional).

- 14 of 16 growth-room respondents are past exploration with agentic AI; 5 run agents in production across the business (base 16, directional).

- Half of charging AI founders price on usage and 18 percent on outcomes, against 25 percent mentioning per-seat; 1 in 10 founders now name finance as their buyer (bases 44 and 49, any-mention).

- The seat gap: inside companies the CEO is the most named AI signer at 47 percent; from outside, founders name the CIO or CTO at 47 percent and the business unit at 35 percent as who they sell to (bases 76 and 49).

- The vertical split: 21 of 28 enterprise-software founders sell to the CIO or CTO; 7 of 8 fintech founders price on usage or outcomes; 2 of 10 healthcare founders are not yet charging (base 76 sector answers, cells directional).

- Days to hours is the recurring compression reported in the finance sessions: three-statement models from days to hours; full planning models inside a working day; months-long forecasting engagements re-scoped to days (finance peer-learning sessions, qualitative).

- Several times the estimate: audits of live AI data connections in the sessions' accounts kept finding multiples of what IT leadership believed was running, the sharpest governance pattern in the rooms (generalized from individual accounts).

Defensible Claim Language

True the day this edition ships, phrased to survive scrutiny and to be quoted with attribution to Open Future Forum:

- “In 2026, 421 executives answered Open Future Forum's AI instrument questions through applications to seven events, spanning finance, security, growth, and founder rooms.”

- “Among Open Future Forum finance-room respondents, proving ROI is the most named blocker to further AI spend (53 percent, base 76), and 62 percent expect measurable return in under 6 months.”

- “One in six Open Future Forum finance-room respondents funds this year's AI budget at least partly from money that would otherwise have gone to headcount (base 76).”

- “In the Open Future Forum network, the CEO is the most named signer of AI purchases inside companies, while founders selling in most often name the CIO or CTO: the seat gap.”

- “Operators in Open Future Forum's finance peer-learning sessions report AI compressing core finance work, including modeling, reconciliation, and reporting, from days to hours.”

Avoid: describing the survey figures as a poll of attendees, they are applicant-pool answers; presenting the Executive AI Leverage Ladder as a measured distribution before the instrument reports; quoting any figure without its base; and calling the peer-session material a survey. Accurate verbs for the sessions: convened, observed, reported by participants.

The Thesis, in One Line

The data says the network is deployed, gated on proof, and expected to show return inside six months, with the pen and the accountability in different seats. The rooms say the executives clearing that gate are the ones treating cost, governance, and process design as parts of the craft.

What We Will Measure

Part one's survey items continue to field at every event. The instrument below adds what this preview's qualitative layer showed is missing, and it defines the bar for Edition 1: the flagship Ladder Stage reading and the headcount-posture reading, each on a finance-tagged base of at least 40. When those numbers exist, they lead Edition 1; until then, this program does not publish them. It is asked of operating executives about the function they lead, and reported role-tagged with the base stated.

The Flagship Reading: Ladder Stage

In the function you lead, AI today is mainly: a thought partner that speeds up my own work (productivity) / a co-worker that completes whole tasks or workflows (capability) / a system that surfaces questions and issues before we ask (context) / not yet material. The Executive AI Leverage Ladder reading is the distribution across the four, and it is built to be longitudinal: the same question, the same rooms, tracked edition over edition, overall and by lane, until it stands as the benchmark reading for executive AI leverage.

Supporting Readings

- Compression. Name the single piece of work AI has compressed most, and the before and after duration, in bands. Reported as a distribution of compression ratios.

- Headcount posture. Over the next 12 months your team will: grow / hold flat with growing scope / hold flat with flat scope / shrink. The flat-with-growing-scope share is the lived leverage line.

- Craft adoption. Which of the following are true in your function: usage limits set and reviewed / routine work routed to cheaper models / repeatable work captured as reusable skills or agents / deterministic automation used where accuracy is non-negotiable / an inventory of AI data connections exists. Reported as counts of five, a simple craft-maturity score.

- Governance exposure. Do you know, within 20 percent, how many AI data connections are live in your organization: yes / no / no, and it worries me.

- Revenue use. Is AI in your function used on the revenue or cash side (contracts, collections, deal review), the cost side, or both.

Collection follows the house rules: fielded at executive events from July 2026 onward, answered by operating executives only for the headline figures, no figure published below 40 responses in a cell, and early reads below that floor labeled directional.

What This Is, and What It Is Not

This is a preview: the first output of a live instrument, not the settled findings of a mature one. It is a two-layer read from a screened community of operators: survey data with the base on every figure, and a close read of practice from the people doing the work, on the record with peers, not respondents to a panel they will never meet. The value is proximity, and the claims are written to be checked.

Two of its constructs appear to be original, stated as checkable claims. The established maturity frameworks, Gartner's AI maturity model and MIT CISR's enterprise AI stages among them, measure the organization; the Executive AI Leverage Ladder measures the executive's own working relationship with AI, a different instrument for a different reader. And no published research this program can find pairs who signs AI purchases inside companies with who the founders selling in actually target; the seat gap is, as far as we can establish, a first read. If either claim is shown to have prior art, the next edition will say so at the claim.

It is not yet a benchmark, and it is not a market estimate. The benchmark is the ambition: a recurring, role-tagged, floor-governed reading of executive AI leverage that this preview baselines and later editions earn. The survey rooms self-selected into AI-themed events and are role-mixed, and the peer-learning sessions are small rooms of practitioners screened for being ahead of the curve; neither says what executives in general do, and this report never claims they do. It sits beside the large annual studies, and beside Open Future Forum's own budget-and-buying Index, as the operator's-eye companion: the big reports say how much is being spent, the Index says who is buying and why, and this report says where executives stand and what the leverage actually is when someone gets it.

Methodology and Honesty Notes

Part one's figures are drawn from instrument questions embedded in the application flow for seven Open Future Forum events in 2026, with 421 applicants answering at least one instrument question; the figures therefore describe applicant pools rather than confirmed attendance. The bases: finance buying stage, 185; the combined finance budget, sign-off, blocker, and return-expectation questions, 76; the CISO Roundtable questions, 16; the agentic go-to-market stage question, 16; founder buyer and pricing questions, 49 and 44; founder sector answers, 76, self-described in free text and classified by us into verticals, with multi-sector answers counted in each and cross-tab cells of 5 to 28 reported as counts. Several questions allowed multiple selections, and percentages for those are any-mention, so they can sum past 100; every chart states its base and these conventions on its face. Bases below the program's 40-response floor are labeled directional wherever they appear.

Part two's source is Open Future Forum's facilitated finance peer-learning sessions in 2026, small rooms of finance leaders across staffing, healthcare, insurance, investment, SaaS, and accounting, approved from larger applicant pools specifically for being active practitioners. Sessions are held under Open Future Forum's community confidentiality norms. This report publishes only generalized patterns from them: no participant is named, no company is identified, and identifying details from individual accounts, including company sizes, role tenures, and specific counts, are removed or generalized so that no account can be traced to a person or an organization. Quotes attributed to Murray Newlands and marked as session remarks are his own words in session, lightly edited for written clarity without changing meaning; quotes attributed to him as founder of Open Future Forum are his statements of this report's findings, and the figure notes beneath them carry the underlying bases.

Five limits are stated plainly. First, the sessions are small rooms: patterns from them are hypotheses for the instrument to test, not measurements. Second, both the session participants and the survey respondents self-selected into AI-themed events, so they over-represent the leading edge on purpose; nothing here describes the median team. Third, compression figures and savings claims are participants' accounts of their own work, consistent across independent tellings but unverified by us. Fourth, the survey rooms are role-mixed, drawing operators alongside founders, investors, advisors, and vendors, so survey figures describe the rooms, not clean panels of the title on the door. Fifth, the community skews toward the San Francisco Bay Area technology economy, and practices may transfer unevenly to other industries and regions.

Data availability. The record-level data behind these figures, including application answers and session material, is not published, to protect applicant and participant privacy. Findings are published in aggregate only, with the base stated at every figure, and that is the form in which this report should be cited.

Independence and Disclosure

Open Future Forum runs the events and sells sponsorships, and Murray Newlands does fractional advisory work with AI companies, including work adjacent to finance teams. Sponsors and partners do not see, shape, or approve the analysis or the findings. This report names no vendors for ranking or recommendation; where a category of tool is described, it is because operators in the rooms described using or wanting it. Any company connected to Open Future Forum or Murray Newlands that appears in this report is disclosed as such. Participant identities and contact data are not shared with sponsors. This statement runs in every edition.

About

Open Future Forum is a private executive community that convenes finance, security, and growth leaders across a program of invitation-screened dinners, gatherings, and peer-learning sessions, including the CFO Executive Forum, the CISO Executive Forum, and related peer groups. Its operator-level research runs on two tracks: the Enterprise AI Buying & Budget Index, which reads how executives fund and buy AI, and the Executive AI Leverage Report, which reads where they stand and how they use it.

Murray Newlands is the founder of Open Future Forum. He is the author of Online Marketing: A User's Manual (Wiley) and a Fellow of the Royal Society of Arts. He writes Murray's Newsletter on AI, venture, and enterprise strategy.

More at openfutureforum.com.

Suggested Citation

Open Future Forum, The Executive AI Leverage Report, Preview Edition, July 2026. Figures from this edition may be cited as the Open Future Forum baseline readings, July 2026. Short handle for repeat reference: the Executive AI Leverage Ladder. The report is a recurring series, released as the material supports rather than on a fixed schedule. This preview precedes Edition 1, which ships when the flagship Ladder Stage and headcount readings clear the 40-response, role-tagged floor. Each release carries its designation and date, lives at a stable URL, and stays published so the ladder can be tracked from its first read.

Sources

First-party sources. Instrument questions embedded in the application flow for seven Open Future Forum events in 2026 (421 responses), including the Claude for Finance event, the AI as a Force Multiplier finance event, the CISO Roundtable Dinner, the Agentic AI Meets Go-to-Market event, and the YC founder events; and Open Future Forum's 2026 finance peer-learning sessions, published here as generalized patterns only.

External benchmarks, attributed where cited and used for context only. The two primary external data sources link to the original reports; other sources link to the publisher, where the specific release can be found.

- Boston Consulting Group. BCG AI Radar 2026: As AI Investments Surge, CEOs Take the Lead. Survey of 2,360 executives including 640 CEOs; CEO AI decision-making. bcg.com

- Gartner. Forecasts on finance headcount-growth expectations. gartner.com

- MIT. The GenAI Divide: State of AI in Business 2025, MIT Project NANDA. Generative AI pilot outcomes and measurable profit. mit.edu

- MarketsandMarkets. Agentic AI Security Market, Global Forecast to 2032. Market size and growth rate. marketsandmarkets.com

- Deloitte. Enterprise AI adoption by industry. deloitte.com

- McKinsey & Company. Research on enterprise AI adoption and value capture by industry. mckinsey.com

- NVIDIA. State of AI 2026. Industry adoption and return. nvidia.com

- S&P Global Market Intelligence. Survey data on companies abandoning AI initiatives, 2025. spglobal.com

- Stanford Digital Economy Lab. Research on entry-level employment in AI-exposed occupations, 2025. digitaleconomy.stanford.edu

- Klarna. Company statements on AI customer service, 2024 to 2025, as widely reported. klarna.com

External benchmarks are used for context only and are current as cited at July 2026; in a fast-moving market, later revisions are expected and will be flagged per the moving-market commitment. They are not affiliated with this report and do not endorse it.

Frequently Asked Questions

This report is published by Open Future Forum for general information and research purposes only. It is not legal, financial, investment, tax, accounting, or other professional advice, and nothing in it is a recommendation to adopt any particular tool, vendor, practice, or course of action. Survey figures describe self-selected, role-mixed rooms with bases stated per figure; practices described are participants' accounts of their own work in a small, self-selected group and may not transfer to other organizations. Readers should do their own research and consult qualified advisors before making decisions. Open Future Forum makes no warranty as to accuracy or completeness and accepts no liability for actions taken in reliance on this report.

© 2026 Open Future Forum. All rights reserved. The Executive AI Leverage Report and the Executive AI Leverage Ladder are works of Open Future Forum. Quotation for journalism, research, and commentary is welcome with attribution to Open Future Forum. All third-party names and marks belong to their respective owners.

Join the Next Session

Private, off-the-record peer-learning sessions for finance leaders comparing live AI deployments. No vendors. No agenda. Just operators.