Executive Summary

Adoption is not transformation, and this report is built on the difference. AI transformation, as measured here, is the move from scattered pilots to AI embedded in how a function runs, and it is visible in four places: spend moving from experimental to core budgets, output decoupling from headcount, whole units of work handed to AI rather than assisted by it, and governance catching up to deployment. A company can run AI tools everywhere and still have transformed nothing. Every finding in this report maps to one of those four markers.

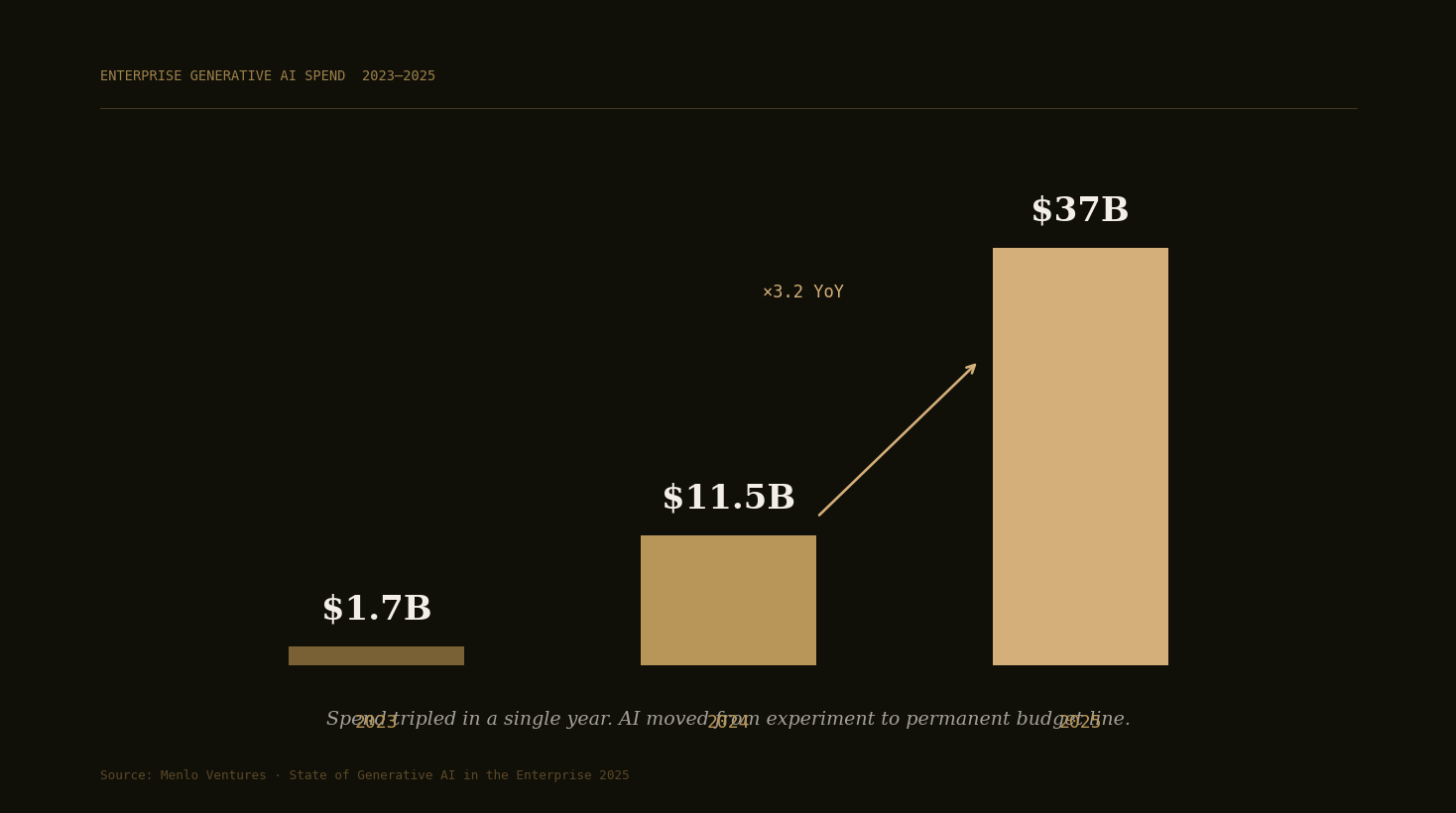

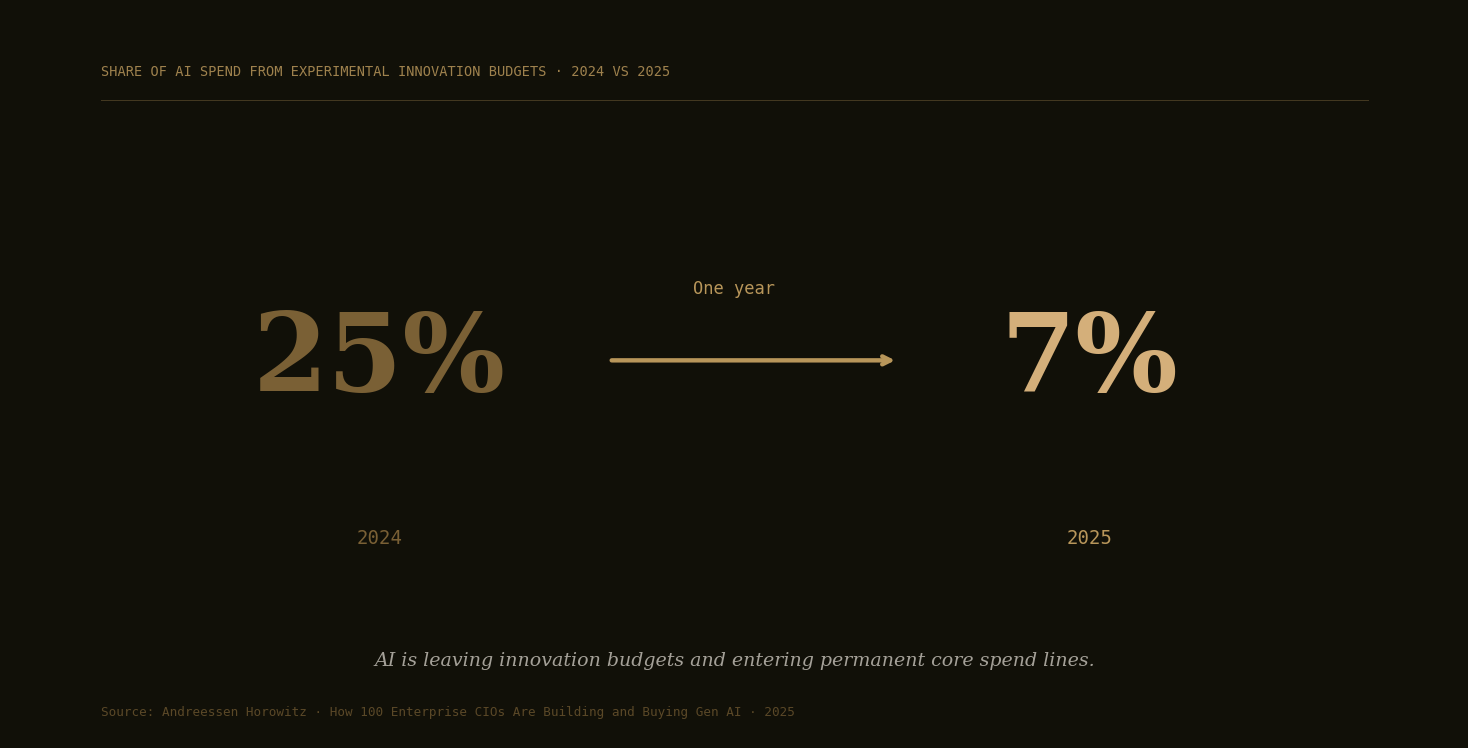

The external picture in 2026 carries both halves of the story. On one side, the money has gone core: enterprises spent $37 billion on generative AI in 2025, a 3.2x rise in a year (Menlo Ventures), innovation budgets collapsed from 25 percent to 7 percent of AI spend (a16z), and 47 percent of AI deals now reach production, nearly twice the SaaS rate (Menlo Ventures). On the other side, the work has not kept up with the wallet: MIT found roughly 95 percent of generative AI pilots produced no measurable profit-and-loss impact, S&P Global found the share of companies abandoning most of their AI initiatives jumped from 17 to 42 percent in a year, McKinsey finds only 7 percent of firms have fully scaled AI, and Gartner expects more than 40 percent of agentic projects canceled by the end of 2027.

Our own rooms show the same tension from the inside, and it is the lead finding of this edition: the transformation gap. The network is deployed. 71 percent of the largest finance room already runs an AI tool (base 185). But the markers lag the deployment. The funding is still mostly net-new rather than reallocated or harvested from headcount (base 87). The sign-off sits with the CEO at 47 percent, far from the workflows being changed. And in the security room, 69 percent govern AI with no dedicated budget line, while 62 percent name securing AI agents as the biggest problem on their desk (base 26, directional). Deployment is real. Transformation, on the markers, is partial.

The flagship metric of this series is the AI Transformation Index: the share of operating executives who say AI is deployed in one or two workflows or embedded in how the function they lead runs. That question is new. It has not yet been fielded, and this edition says so plainly: until it clears the 40-response floor, the buying-stage read above (base 185) is reported as the seed series and closest proxy. Edition 1 sets the baseline. The Index line starts here.

The Answers We Have Now

This section is the data in hand, drawn from Open Future Forum event records across the twelve events in the July 2026 data pull, spanning the finance, security, growth, founder, and investor rooms. Invitation outreach that did not become an application is excluded from every count in this report; the figures count the people who applied. Demand figures are rounded floors of distinct applicants by lane; opinion figures come from the instrument questions in the application flow, with the base on the face of every figure. Each finding below ties to one of the four transformation markers.

Finding 1: The network is deployed, not exploring

Asked where their team is with AI today, 71 percent of the largest finance room said they already run Claude or another AI tool, 22 percent are evaluating, and 8 percent have not started (base 185). The growth room reads further along the agent curve than the label suggests: of 38 go-to-market respondents, 12 are piloting agents in a function or two, 10 are building agentic AI products, 9 are running agents in production across the business, and 7 are still exploring (base 38, reported as counts, below the 40-response floor). Read against the marker of whole units of work, the picture is a network past the starting line: most of it is running AI, and a meaningful slice of the growth room has already handed complete workflows to agents. The demand behind the reads, as rounded floors of distinct applicants: more than 290 founders, more than 270 in the finance rooms, more than 250 in the engineering and data-agent rooms, more than 220 in marketing and growth, 70 in the security lane, and more than 30 investors.

Finding 2: Transformation is still being bought more than harvested

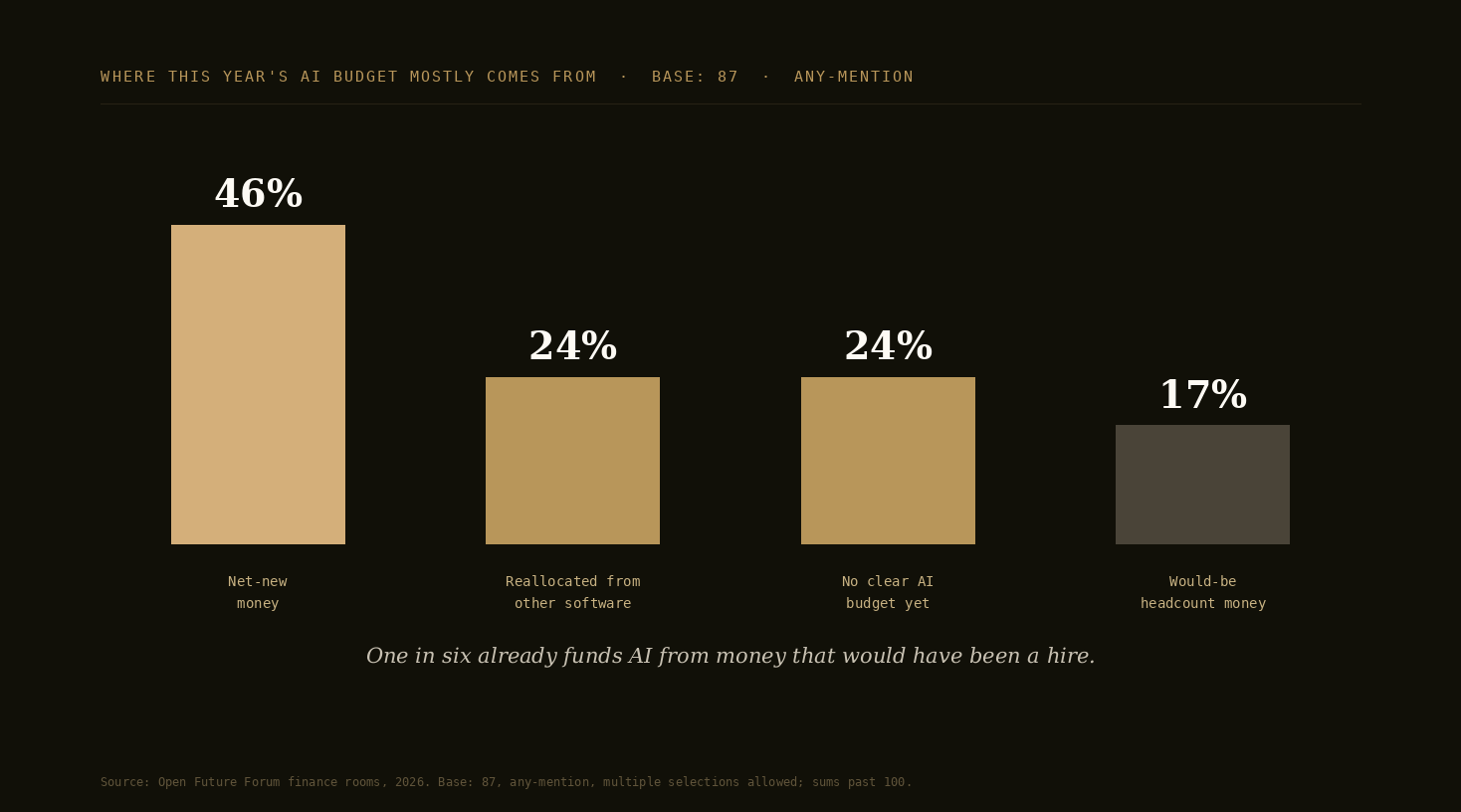

Asked what this year's AI budget is mostly made of, 46 percent of the finance rooms said net-new money, 24 percent said money reallocated from other software, and 17 percent said money that would have gone to headcount; 24 percent have no clear AI budget yet (base 87, any-mention, sums past 100). This is the spend-and-headcount marker, and it reads mid-shift. When AI is transforming a cost structure, its budget comes out of the things it replaces: other software, and hires that no longer happen. In these rooms, roughly one in six funds AI from would-be headcount money and a quarter from reallocated software spend, while net-new money is still the largest single source. The external curve points the same direction from further along: a16z finds innovation budgets have collapsed to 7 percent of AI spend. In our rooms, the money has arrived, but most of it has not yet displaced anything.

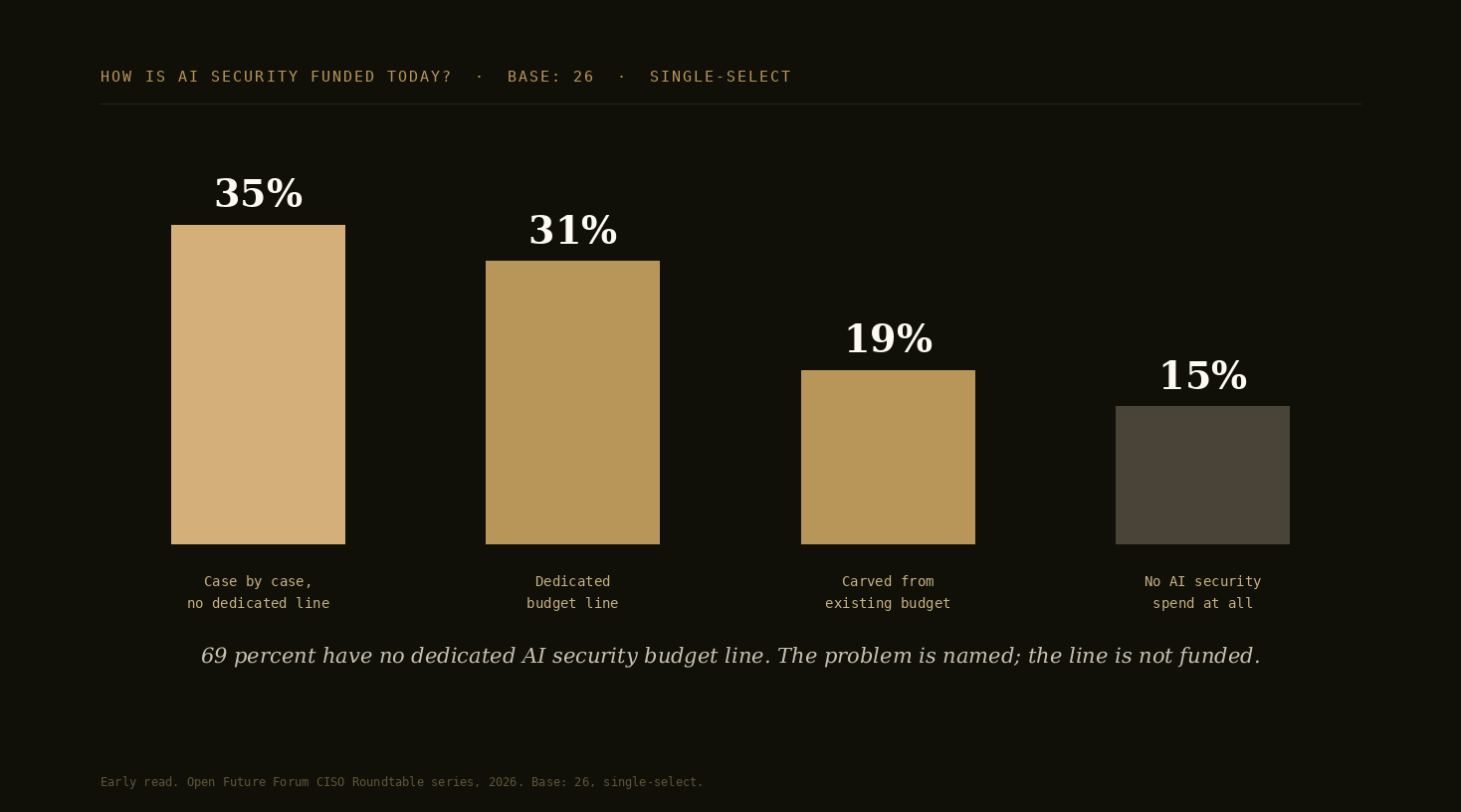

Finding 3: Governance trails deployment

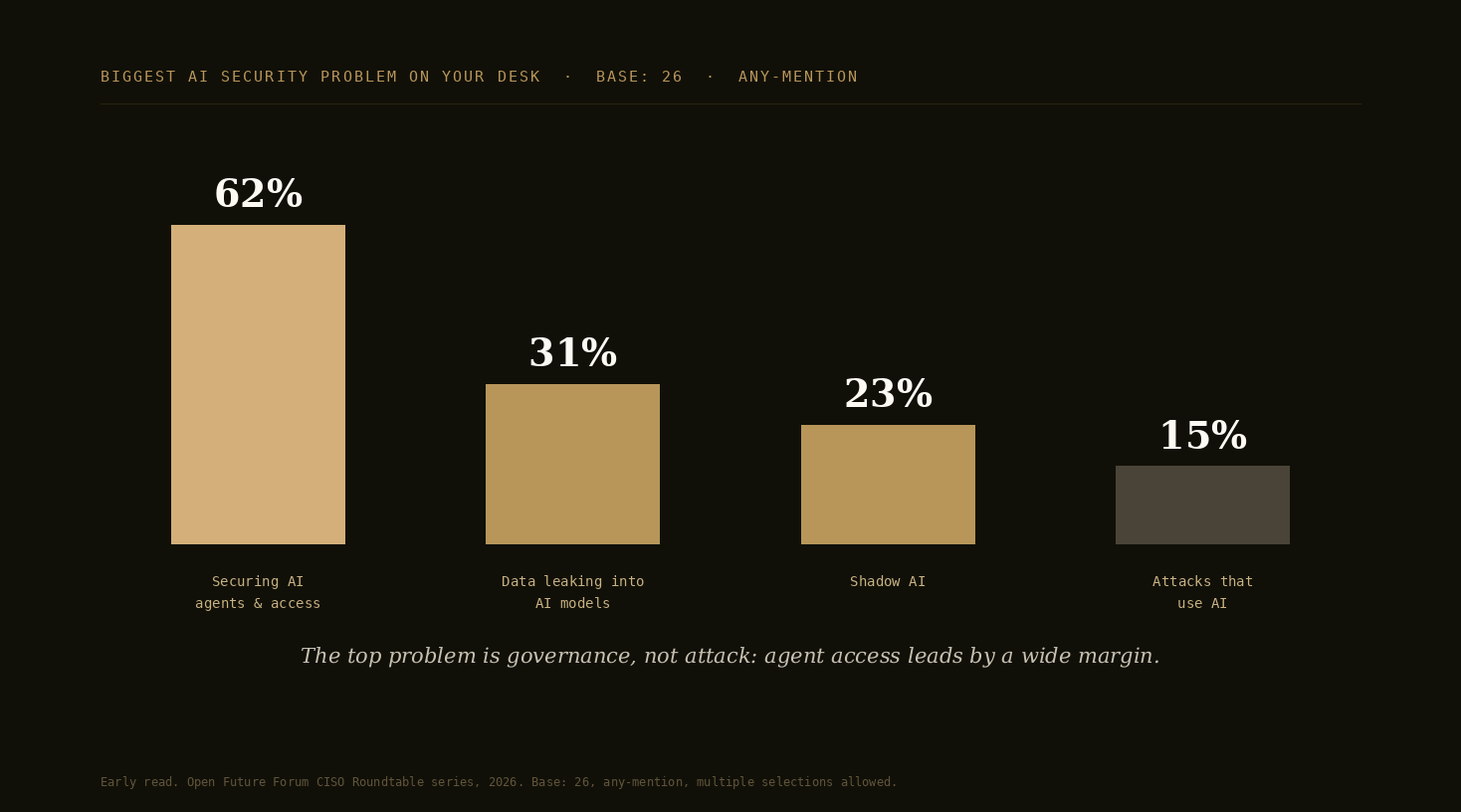

The governance marker is read in the security room, and it lags the rest. Asked the biggest AI security problem on their desk, 62 percent named securing AI agents and their access, ahead of data leaking into AI models at 31 percent and shadow AI at 23 percent (base 26, any-mention). Asked how AI security is funded, only 31 percent said it has its own budget line: 35 percent fund it case by case, 19 percent carve it out of the existing security budget, and 15 percent have no AI security spend at all (base 26, single-select). Put together: 69 percent of the room has no dedicated line for the problem 62 percent name. Among the ten security leaders inside the base, nine of ten have no dedicated line. These are early directional reads, and they describe transformation's trailing edge: the functions deployed the AI, and the governance is still being paid for out of pocket.

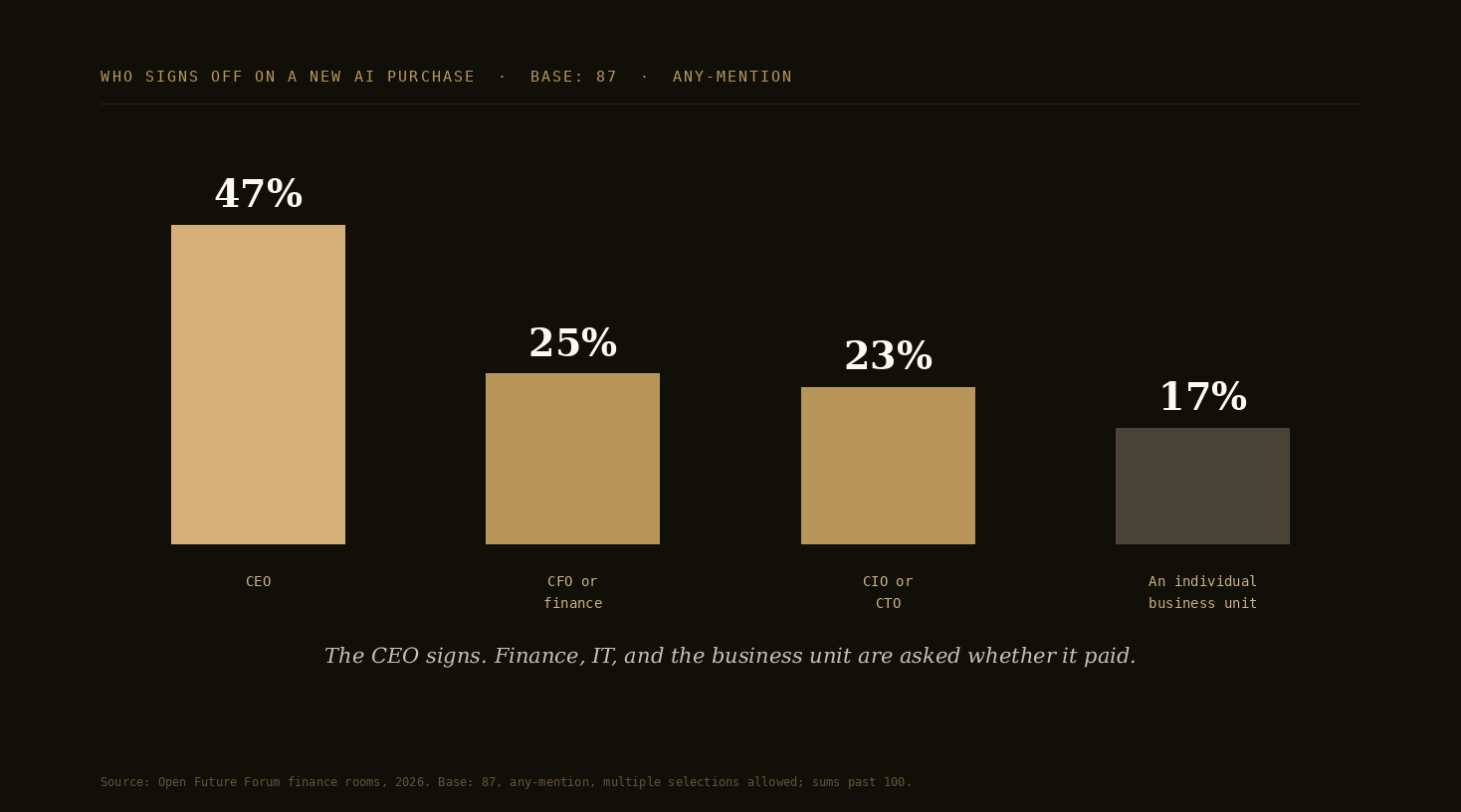

Finding 4: The pen and the proof sit in different seats

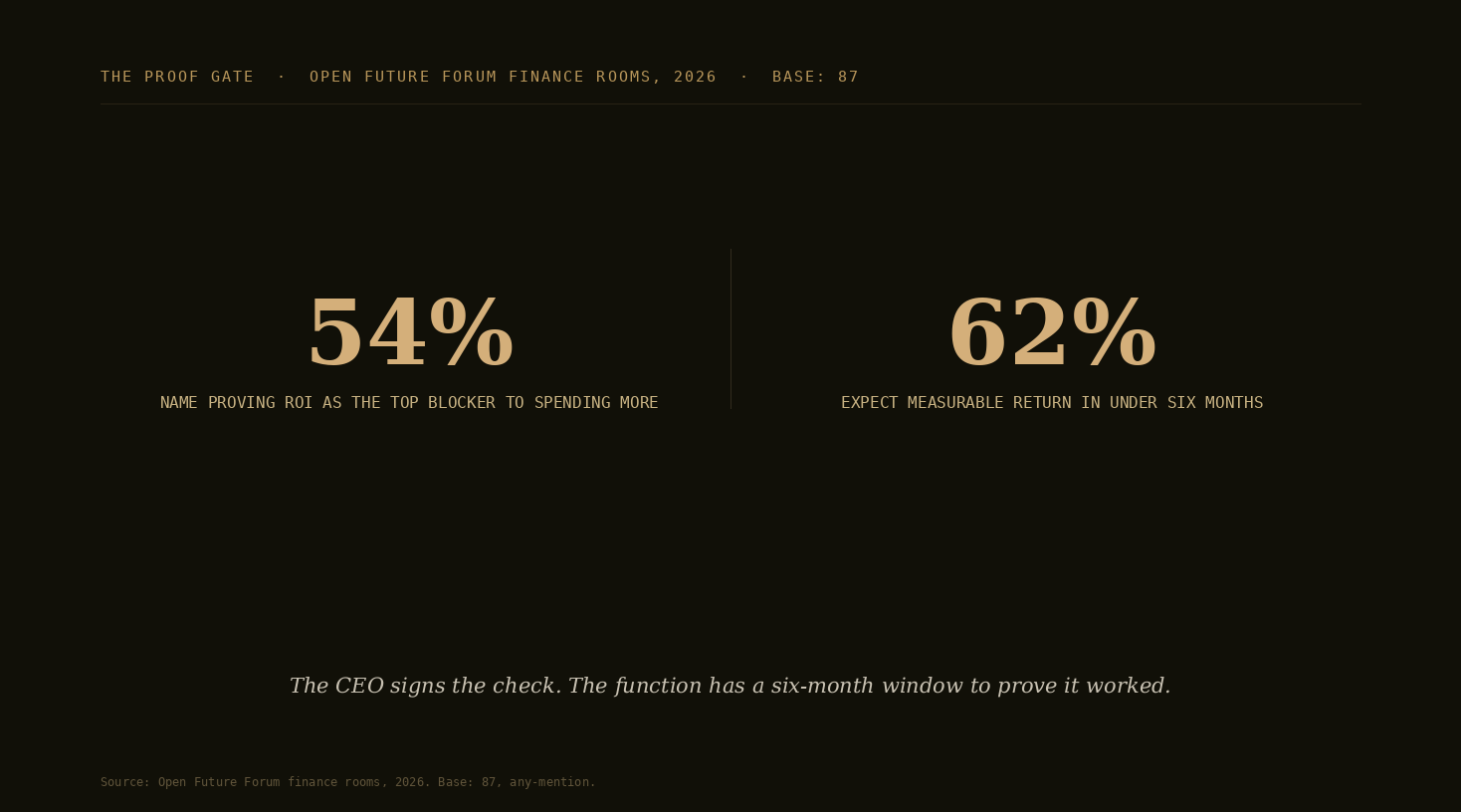

Asked who signs off on a new AI purchase, the finance rooms named the CEO first at 47 percent, then the CFO or finance at 25 percent, the CIO or CTO at 23 percent, and an individual business unit at 17 percent (base 87, any-mention). Asked the main thing stopping them spending more, 54 percent said proving ROI, and 62 percent expect measurable return in under six months. That combination is the governance shape transformation has to survive: the CEO signs the check, the operating function has to produce the proof, and the proof window is short. A transformation that cannot show a measurable result inside six months is, in most of these rooms, a transformation that loses its budget. The proof gate is not a blocker to transformation. It is the filter that decides which transformations are real.

Honesty notes on the counts

- Figures are rounded floors of distinct applicants, kept deliberately conservative. Invitation outreach that did not become an application is excluded from every count, and application is not attendance. Some people apply to more than one event, so lane totals are floors rather than exact unique counts.

- The rooms are role-mixed. The largest applicant block in the network is engineers, and the security and finance rooms include founders, investors, and advisors alongside the operators. Role-tagged cuts are shown where they exist, and applicant counts are never presented as counts of any one title.

- Registration forms collect screening data, not opinions. Accurate verbs for the demand layer: applied, convened, brought together, engaged. Opinion figures come only from the instrument questions, with the base stated.

- The flagship transformation-stage question has not yet been fielded. The buying-stage read (base 185) is the seed series and closest proxy, and it is never presented as the Index itself.

Defensible claim language, from the data in hand

- "The July 2026 Open Future Forum data pull spans twelve events, including more than 290 distinct applicants in the founder rooms, more than 270 in finance, and 70 in the security lane."

- "In the largest Open Future Forum finance room, 71 percent of 185 respondents already run Claude or another AI tool."

- "In the Open Future Forum finance rooms, 46 percent of 87 respondents fund this year's AI budget mostly with net-new money, and 17 percent with money that would have gone to headcount."

Early Signal from the Room

The instrument questions already live in the application flow give this edition its first cross-lane transformation reads. Each carries its base on its face; reads below the 40-response floor are directional, in "we asked; this is what they said" form.

The funding read is the sharpest. Across the finance rooms, net-new money leads at 46 percent, reallocated software money follows at 24 percent, and would-be headcount money sits at 17 percent (base 87, any-mention). On the transformation markers, the second and third numbers are the ones to watch: they are the shares for whom AI spend has started displacing something, which is what a changed cost structure looks like in a budget. Edition over edition, transformation shows up as those two shares rising and net-new falling.

The stage reads sit at different points on the curve by lane. The finance rooms are deployed: 71 percent running a tool, 22 percent evaluating, 8 percent not started (base 185). The growth room is furthest into agents: 9 of 38 run agents in production across the business, 12 pilot them in a function or two, 10 build agentic products, and 7 still explore (counts, base 38). The security room reads the trailing edge: 69 percent with no dedicated line for AI security (base 26, directional). One network, three lanes, three points on the same curve.

The founder rooms supply the supply-side marker. Of 92 founders asked how they charge, 83 are charging, and roughly two thirds of those, 53 of 83, price on usage or outcomes (any-mention). Pricing that meters value only works on transformed workflows: an outcome price assumes the work has been handed over cleanly enough to count the outcomes. The sellers are pricing for a transformation their buyers, on the reads above, have only partly completed.

The investor room is small and read as counts: of 20 investors asked who increasingly owns the AI buying decision across their portfolios, 8 named the CEO, 8 the CIO or CTO, 3 individual teams, and 2 finance, while 5 said it is too early to say. Asked where AI is making the biggest difference, 9 said better products, 7 cutting costs, 7 helping customers, and 4 nothing measurable yet (both base 20, any-mention, directional).

The flagship transformation-stage question defined in this report, together with the supporting metrics on funding, headcount posture, process readiness, and governance, enters the field at upcoming Open Future Forum events across all lanes: finance, security, growth, founder, and investor. The next edition reports the AI Transformation Index on its own responses, overall and by lane, against the seed series printed here. Read this edition's figures as the first points on a line, not as settled numbers.

By the Numbers

The AI transformation shift, in the figures the market is citing in 2025 and 2026. External benchmarks are attributed to their sources and used for context. The Open Future Forum figures are reads from our own rooms, with the base shown.

- $37 billion, enterprise spend on generative AI in 2025, up 3.2x in a year, with 47 percent of AI deals reaching production, nearly twice the traditional SaaS rate (Menlo Ventures).

- 25 percent to 7 percent, the one-year collapse in the share of enterprise AI spend drawn from innovation budgets, as AI spend grew roughly 75 percent and moved into core IT and business-unit budgets (a16z).

- 7 percent of firms have fully scaled AI, and 39 percent report any EBIT impact from it (McKinsey).

- Roughly 95 percent of enterprise generative AI pilots produced no measurable profit-and-loss impact (MIT, The GenAI Divide, 2025).

- 17 percent to 42 percent, the one-year jump in the share of companies abandoning most of their AI initiatives (S&P Global Market Intelligence).

- More than 40 percent of agentic AI projects are expected to be canceled by the end of 2027 (Gartner).

- 18 to 20 percent use AI in a business function on the nationally representative read, and 57 percent of adopters run it in three or fewer functions (US Census Bureau, Business Trends and Outlook Survey).

- Three in four enterprise leaders report positive returns on generative AI, with 82 percent using it weekly and 46 percent daily (Wharton Human-AI Research and GBK Collective, a multi-year study of about 800 senior leaders at large US companies).

- 11 percent to 53 percent, the rise in the share of $1 billion-plus US organizations with AI agents deployed between early 2025 and mid 2026, while only 26 percent have full real-time visibility into what their AI systems cost to run (KPMG AI Quarterly Pulse).

- 6 percent to 2 percent, the fall in finance leaders' expected headcount growth as AI absorbs the work (Gartner).

- 72 percent of CEOs call themselves the main AI decision-maker (BCG AI Radar 2026, a survey of 2,360 executives).

- $1.65 billion to $13.52 billion, the forecast growth of the agentic AI security market from 2026 to 2032, a 42 percent compound annual rate (MarketsandMarkets): the market pricing the governance gap.

From our own rooms, with the base shown:

- 71 percent of the largest finance room already runs Claude or another AI tool (Open Future Forum finance rooms, base 185).

- 46 percent fund this year's AI budget mostly with net-new money; 17 percent with money that would have gone to headcount (Open Future Forum finance rooms, base 87, any-mention).

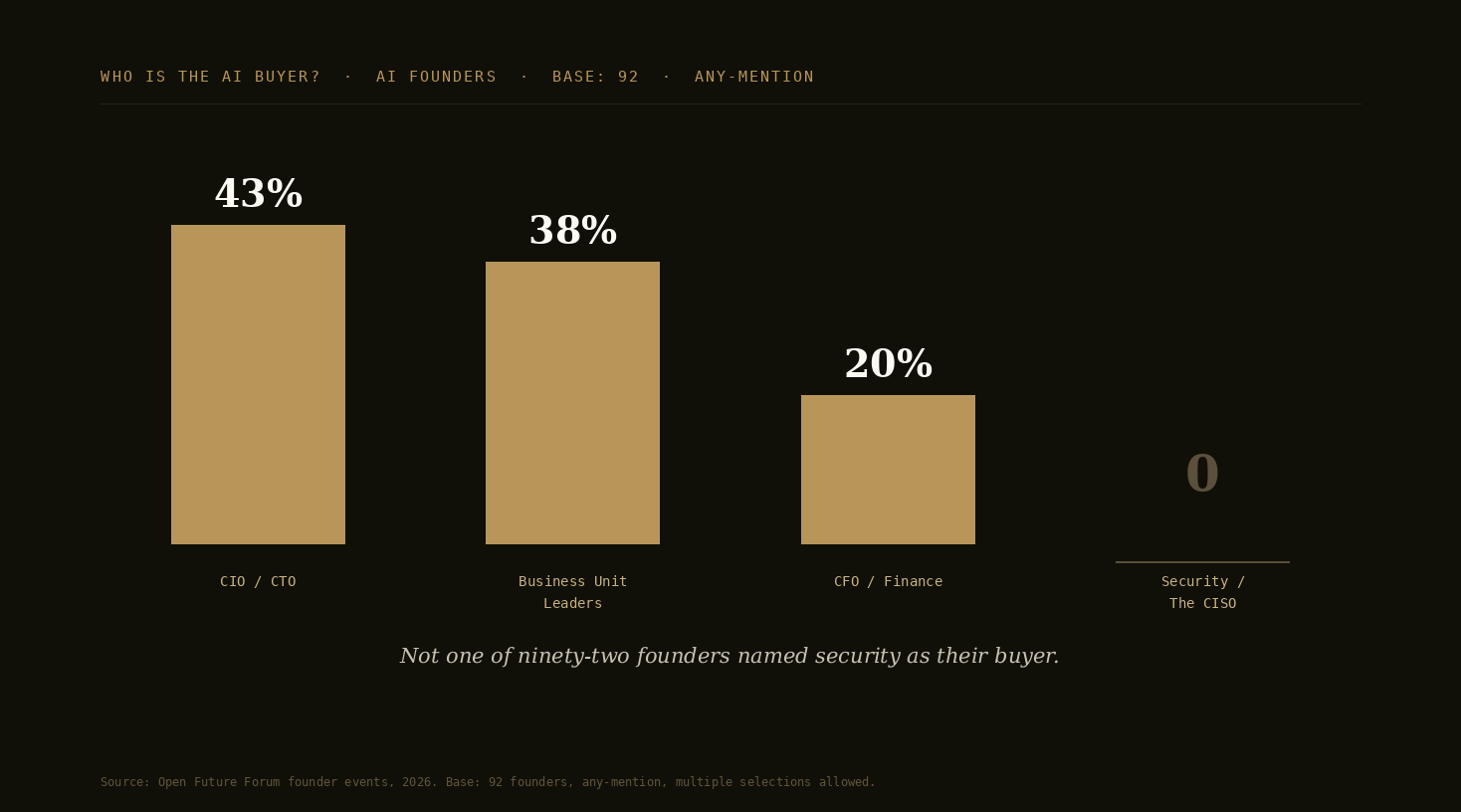

- 69 percent of the security room has no dedicated budget line for AI security, while 62 percent name securing AI agents and their access as the top problem (Open Future Forum security rooms, base 26, directional).

- Roughly two thirds of charging founders price on usage or outcomes: 53 of 83 (Open Future Forum founder events, base 92, of whom 83 charge, any-mention).

The Thesis, in One Line

Transformation is not adoption. It is the point where the spend goes core, the output decouples from headcount, and the governance catches up, and the rooms show all three lines moving at different speeds.

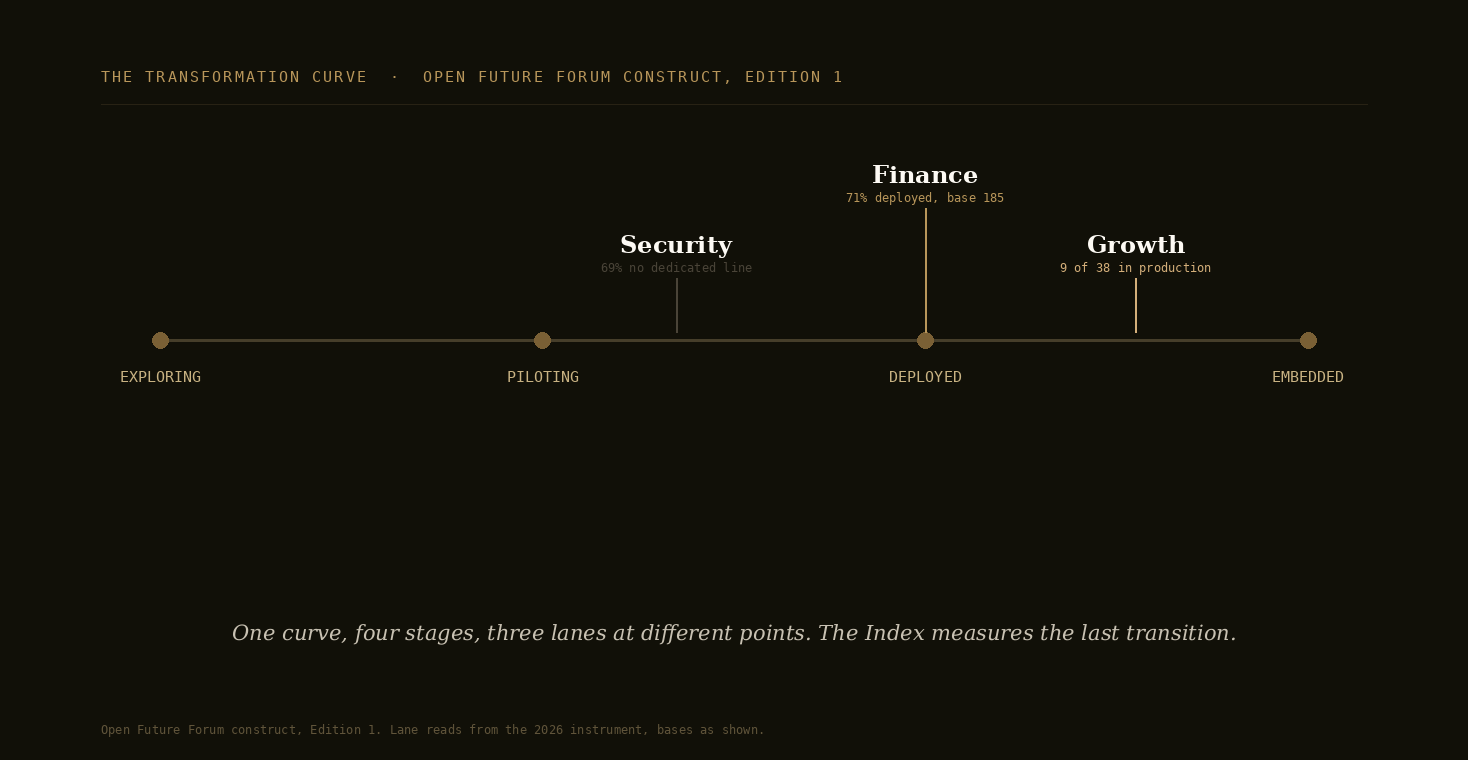

The Transformation Curve

This report reads every stage figure against a simple four-stage curve, defined here as this report's own construct and carried forward as the frame later editions track: exploring, piloting, deployed, embedded.

Each transition is distinguished by one marker. From exploring to piloting, the marker is spend: real money is committed, usually experimental. From piloting to deployed, the marker is work: a live workflow runs on AI, in production, not in a sandbox. From deployed to embedded, the markers converge: the spend moves to core budgets, whole units of work are handed over rather than assisted, output starts to decouple from headcount, and governance stands up around what is running. Embedded is the stage at which removing the AI would change the function's cost structure or hiring plan. That last transition is the one the AI Transformation Index is built to measure, and it is the one most of the market has not yet made: McKinsey's 7 percent fully scaled is the external estimate of the embedded stage.

Mapped onto the curve, the lanes sit apart. The finance rooms sit at deployed: 71 percent run a tool, but the funding mix says the spend has not fully gone core. The growth room straddles deployed and embedded: 9 of 38 run agents in production across the business. The security room marks the trailing edge: whatever stage the other functions reach, 69 percent govern it on ad hoc money. One shape, three points on it, and the gap between the leading lane and the governance behind it is this edition's lead finding.

What Transformation Looks Like Across the C-Suite

Transformation is one shift seen from nine seats, and the seat that signs is not the seat that proves. This section reads the same shift from each chair, using the first-party figures where they exist and saying so where they do not.

The CEO

The seat that signs the most and sits furthest from the practice. The CEO is the most named signer of AI purchases in our finance rooms at 47 percent (base 87), consistent with BCG's finding that 72 percent of CEOs call themselves the main AI decision-maker. The ambition is set at the top; the workflow changes happen several layers down; and the distance between the two is where transformation stalls.

The CFO

The fullest data profile in this edition: 71 percent of the largest finance room deployed (base 185), a funding mix still led by net-new money, proving ROI as the top blocker at 54 percent, and 62 percent expecting return inside six months (base 87). The CFO runs the proof gate that decides which transformations survive, and increasingly funds AI out of money that would have been headcount, which is the harvesting stage of the curve arriving in the budget.

The CIO or CTO

The door the market knocks on. Inside companies the CIO or CTO signs at 23 percent (base 87); outside, founders selling in target the seat at 43 percent, more than any other (base 92). The technology seat admits most of the AI the rest of the company then has to embed and govern, which makes it the throughput constraint of the whole curve: transformation moves at the pace of what this seat integrates.

The CISO

Governance is the price of everyone else's transformation, and it is being paid case by case. In the security room, 62 percent name securing AI agents and their access as the top problem while 69 percent have no dedicated AI security budget line, and nine of the ten security leaders in the base have none (base 26, directional). Every function that reaches the embedded stage adds surface this seat must govern, mostly on money it has to argue for one purchase at a time.

The CMO and growth leader

The furthest along on agents in our rooms: 9 of 38 go-to-market respondents run agents in production across the business, and another 12 pilot them (base 38, counts). Marketing's proof gate is attribution: agents act in public, on customer data, in the brand's voice, so the function that transformed fastest is also the one where measurement has to catch up fastest.

The business-unit leader

The shadow buyer. Named by 38 percent of founders as their target and by 17 percent of finance-room respondents as the internal signer, the business unit buys closest to the work and furthest from the inventory. That makes it both the fastest route to a transformed workflow and the main source of the ungoverned surface the security room reports.

The CAIO

The newest seat, created for the transformation and funded without a baseline. Where a chief AI officer exists, the role owns the curve itself: which functions move to which stage, in what order, against what proof. But the seat has no legacy budget to reallocate from, so its spend is net-new by construction, which is why the funding mix in the finance rooms will read partly as the CAIO's arrival.

The board

The board question has changed shape in a year: from whether the company is adopting AI to whether anyone can state, within bounds, how far the functions have moved and what the spend is displacing. The four markers in this report are a board agenda in miniature: where is the spend coming from, what is the headcount plan, which work has been handed over, and who governs it.

Two seats outside the company, inside the same picture

The AI founder. The supply side prices ahead of its buyer. Of 92 founders asked who owns the buying decision inside the companies they sell to, the CIO or CTO leads at 43 percent and the business unit at 38 percent, with finance at 20 percent and security named by none (base 92, any-mention). And of the 83 charging, roughly two thirds price on usage or outcomes. That pricing assumes a transformed workflow on the buyer's side: outcomes can only be metered where the work has actually been handed over. The founders are selling the embedded stage to buyers who are mostly at deployed.

The venture investor. Concentration is the supply-side mirror of consolidating spend. In our own room of 20 investors, the CEO and the CIO or CTO tie at 8 mentions each as the seat that increasingly owns the AI buying decision, and 5 say it is too early to call (base 20, counts, directional). Capital in 2026 is concentrating on what proves out, which is the same discipline the proof gate applies inside companies: the market and the CFO are running the same filter from opposite ends.

The Same View, by Industry

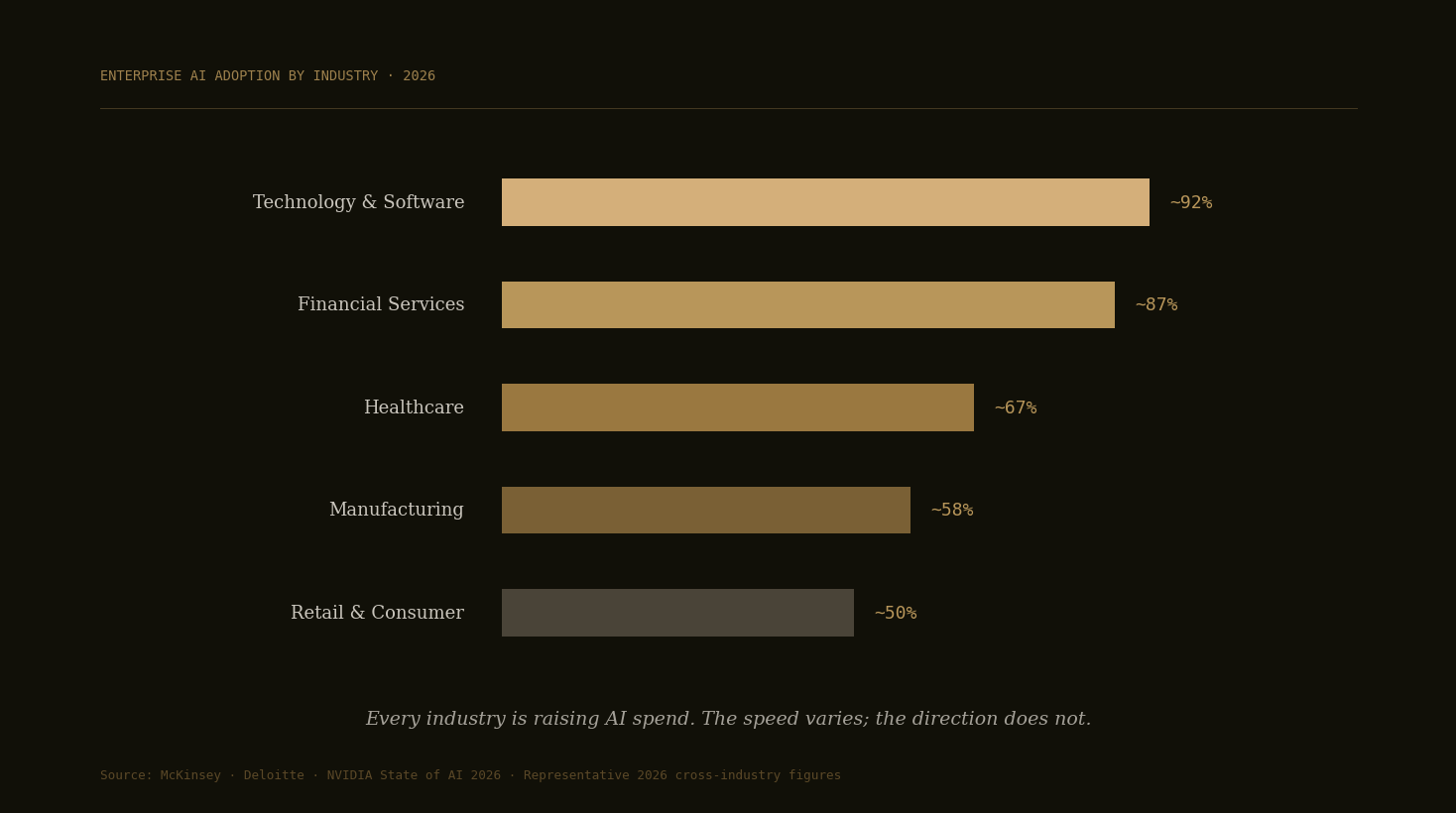

Open Future Forum does not yet run industry-specific transformation rooms, so this read is drawn from external benchmarks, attributed to McKinsey, Deloitte, and NVIDIA, with figures representative of 2026 cross-industry surveys. What changes by industry is not the transformation question but the speed of the answer.

Financial services

Among the most adopted and best-proven AI industries, around 85 to 89 percent on Deloitte's numbers, with regulation acting as both brake and rail. Model risk management existed before generative AI did, so the governance marker arrived early here; the live work is extending frameworks built for models that score to agents that act. Where the proof case is clean, whole units of work in operations and compliance are moving first.

Technology and software

The highest adoption of any sector, around 92 percent, and the furthest along on decoupling: coding is the largest single line of AI application spend, and engineering organizations are the first place output visibly separates from headcount. The sector's transformation risk is cost discipline rather than capability, as the 2026 wave of usage caps showed.

Healthcare and life sciences

The fastest accelerator, climbing from roughly 38 percent adoption in 2024 to about 67 percent in 2026 as regulatory clarity arrived. Healthcare gates on the way in: compliance review runs before deployment, so transformation is slower but better inventoried, and the governance marker leads rather than lags. The lesson travels to every regulated function.

Manufacturing and industrials

Around half to two thirds of firms, with the cleanest cost-out case and the most physical processes. Transformation here means AI reaching into operational technology: predictive maintenance, quality, supply chain. The spend case is strong and the process-readiness bar is high, because handing work to AI on a factory floor requires documentation most workflows do not have.

Retail and consumer

Among the highest adopters of agentic AI, close to half of firms, with agents closest to the customer and the transaction. Transformation shows up in revenue workflows first, pricing, personalization, service, which means the proof gate clears fastest and the governance question arrives as a revenue-protection question. Fast in, fast measured, fast funded.

What AI People Say About Transformation

The commentary around AI transformation split into a sharp, useful debate across 2025 and 2026, and this report carries both sides. One convention first: where a vendor-published statistic would carry weight, this report says who published it and what they sell, and prefers analyst, academic, and benchmark sources.

The reckoning

The skeptic case is that deployment ran ahead of transformation, and the record supports it. MIT found roughly 95 percent of enterprise generative AI pilots produced no measurable profit-and-loss impact. S&P Global found the share of companies abandoning most of their AI initiatives jumped from 17 to 42 percent in a year. Gartner expects more than 40 percent of agentic projects canceled by the end of 2027. The mood has a name, pilot purgatory: tools everywhere, changed cost structures almost nowhere. The cautionary tales are specific. Uber exhausted its annual AI coding budget in four months and answered with per-employee monthly caps on agentic coding tools (Bloomberg), the clearest public case of spend arriving before the controls. And Klarna, after publicly replacing customer service work with AI, moved to bring human agents back into the loop, the caution that transformation is not a straight line and can be walked partway back.

The counter-case

The builders and their backers read the same market as a shakeout, not a failure. Enterprise AI spend hit $37 billion in 2025, up 3.2x (Menlo Ventures), and it is still climbing as it consolidates. 47 percent of AI deals reach production, nearly twice the traditional SaaS rate (Menlo Ventures). Innovation budgets collapsed to 7 percent of AI spend because the money moved into core budgets, not out of the category (a16z). And pricing is arriving that only works when the work is real: outcome and usage pricing, Intercom's per-resolution model among the visible examples (a vendor's own pricing, cited as a market signal rather than a benchmark), meters value instead of seats. And the buyer side has its own rebuttal to the pilot-failure narrative: Wharton's multi-year study of about 800 senior leaders finds three in four reporting positive returns on generative AI, a differently built read that points the other way from MIT's. Capital is concentrating on what proves out.

The reconciliation

The two sides describe one market at one moment. Spend rising and consolidating at once is what a market does when accountability arrives: the proof gate that 54 percent of our finance rooms named as the top blocker is the same filter S&P Global's abandonment number records from the outside. The reckoning is the sound of undifferentiated pilots being cleared; the counter-case is the sound of the survivors going core. The four transformation markers in this report are how the survivors are chosen: spend that displaces, output that decouples, work that is handed over whole, and governance that stands up around it. Both camps are right about their half of the curve.

The Evidence Behind the Theses

The report rests on five theses. Here is how each holds up, support and counter-evidence, so the claims are calibrated rather than asserted. External figures are attributed and used for context; they are not Open Future Forum findings.

Thesis 1: AI spend has moved from experimental to core budgets. Well supported.

Support. Innovation budgets fell from 25 percent to 7 percent of enterprise AI spend in a year while total spend grew roughly 75 percent (a16z), and enterprise spend hit $37 billion at a 3.2x growth rate with 47 percent of deals reaching production (Menlo Ventures). In our own rooms, 24 percent already fund AI by reallocating from other software (base 87).

Counter. Core-budget money is a marker of transformation, not proof of it: money can go core while the work stays assisted. Our own funding read still shows net-new as the largest single source, which is why this report treats the spend marker as necessary but not sufficient.

Thesis 2: AI is beginning to decouple output from headcount. Partially supported, stated carefully.

Support. Gartner finds finance leaders' expected headcount growth falling from 6 to 2 percent as AI absorbs the work, and in our rooms 17 percent already fund AI with money that would have gone to headcount (base 87). The growth room's 9 of 38 running agents in production across the business is decoupling in miniature.

Counter. MIT's roughly 95 percent of pilots with no measurable profit-and-loss impact and McKinsey's 39 percent seeing any EBIT impact say most companies cannot yet show the decoupling on a financial statement, and the US Census Bureau's AI supplement finds AI-related employment decreases in only 2 percent of firms. The Index's Headcount Posture metric is built to measure it directly rather than infer it.

Thesis 3: Deployment is running ahead of governance. Supported first-party, and directionally.

Support. In our security room, 62 percent name securing AI agents and their access as the top problem while 69 percent have no dedicated AI security budget line, nine of ten security leaders among them (base 26, directional). The market is pricing the same gap: the agentic AI security market is forecast to grow from $1.65 billion to $13.52 billion by 2032, a 42 percent compound rate (MarketsandMarkets). KPMG's quarterly pulse of large US organizations shows governance chasing deployment: human validation of agent outputs rose from 22 to 63 percent in a year, yet only 26 percent have real-time visibility into AI operating cost.

Counter. The base is 26 and self-selected into an AI-security-themed room, and a dedicated line is not the only honest way to fund governance. The Governance Read in the instrument tracks the gap over editions rather than asserting it from one read.

Thesis 4: Pricing is moving to usage and outcomes, the supply-side transformation marker. Well supported.

Support. Roughly two thirds of the charging founders in our rooms, 53 of 83, price on usage or outcomes (base 92, of whom 83 charge). Gartner expects at least 40 percent of enterprise software spend to shift to usage, agent, or outcome pricing by 2030, and visible vendor moves such as Intercom's per-resolution pricing point the same way.

Counter. Usage pricing can also just be cost pass-through in a token-metered market, and 2026's spending caps showed buyers pushing back on unmetered burn. The share of AI spend on usage or outcome pricing enters the rotating instrument so the demand side of this thesis gets its own read.

Thesis 5: Most of the market is still mid-curve. Well supported, and the honest counterweight.

Support. McKinsey finds only 7 percent of firms have fully scaled AI. Gartner expects more than 40 percent of agentic projects canceled by end 2027. S&P Global's abandonment jump from 17 to 42 percent records the clearing of the pilot backlog, and the US Census Bureau's nationally representative read puts firm-level AI use at 18 to 20 percent. Our seed series sits far ahead of that baseline, which is the selectivity of the rooms speaking, and it matches the shape: deployed is the mode, embedded is not.

Counter. Mid-curve is a moving position: the same benchmarks showed the market a full stage earlier a year ago. This thesis is the baseline the Index exists to move against, and later editions will report whether the embedded share is actually rising.

Where this leaves the report: it leads on Theses 1 and 3, which carry the strongest support on stated bases, states 2 and 4 in their careful form, and treats 5 as the honest baseline the whole series measures against.

About This Report

The AI Transformation Report is a standalone Open Future Forum research report. It reads how far the operating executives in the Open Future Forum community have moved AI from pilots into the way their functions run, across the finance, security, growth, founder, and investor rooms. This is Edition 1, and each edition carries its own number so the AI Transformation Index line can be tracked over time.

What This Is

A recurring read on one question, asked of the operating executives in the Open Future Forum community: how far has AI moved into the way the function you lead actually runs. It is built on rooms most people cannot reach: invitation-screened dinners and gatherings where the same operators return event after event, so their answers can be tracked over time. The flagship number is the AI Transformation Index, a measured line on the deployed-to-embedded transition, read at the operator level, edition over edition. That number belongs to no one else yet.

What This Is Not

This is not a market-size estimate: it makes no total-spend claims of its own. It is not a maturity certification: no company is scored, ranked, or graded. And it is not a vendor evaluation: it never ranks, scores, or recommends products. The figures describe a small, selective sample of operators inside one community, with the base stated on every figure, and nothing is presented as a probability sample of all enterprises. The value is not scale. The value is that these are the operators actually making the shift, trackable over editions.

The Gap It Fills

The big reports say how much is spent and how fast adoption grows. None reads the transformation markers themselves, spend source, headcount posture, handed-over work, and governance, at the operator level, in the same community, tracked over time. That is the read this series owns.

Definitions

- AI transformation. The move from scattered pilots to AI embedded in how a function runs, visible in four places: spend moving from experimental to core budgets, output decoupling from headcount, whole units of work handed to AI rather than assisted by it, and governance catching up to deployment. Adoption alone is not transformation.

- The four markers. Spend (where the AI budget comes from), headcount (whether output still tracks team size), work (whether complete workflows have been handed over), and governance (whether the AI running is inventoried, funded, and controlled).

- Transformation stage. One of four positions on the curve this report defines: exploring, piloting, deployed, embedded. Embedded means removing the AI would change the function's cost structure or hiring plan.

- Operating executive. A respondent who leads a function: the headline unit for the Index. Answers from advisors, vendors, students, and observers are recorded but not counted in headline figures.

- AI budget. The money a function spends on AI tools, models, and agents in the current year, classified by source: net-new, reallocated from other software, would-be headcount money, or not yet defined.

- Headcount posture. The function's plan for team size over the next 12 months, read against its scope: growing, flat with growing scope, flat with flat scope, or shrinking. Flat with growing scope is the decoupling signal.

- Shadow AI. AI tools in use inside the organization without approval or, often, knowledge. The transformation that does not appear in any inventory.

- The minimum-base rule. No headline figure is published below 40 role-tagged responses. Smaller bases are early directional reads, labeled as such, with the base on the face of every figure.

Questions This Report Answers

What is the AI Transformation Report?

A standalone Open Future Forum operator-research report on how far executives have moved AI from pilots into the way their functions run, read across the finance, security, growth, founder, and investor rooms, with the base stated on every figure.

What is the AI Transformation Index?

The report's flagship metric: the share of operating executives who say AI in the function they lead is deployed in one or two workflows or embedded in how the function runs, changing its cost structure or hiring plan. It is tracked edition over edition, overall and by lane. The question enters the field after this edition; the buying-stage read (base 185) is the seed series.

What counts as AI transformation versus AI adoption?

Adoption is using AI tools. Transformation is AI changing how the function runs, visible in four markers: spend moving from experimental to core budgets, output decoupling from headcount, whole units of work handed to AI rather than assisted by it, and governance catching up to deployment.

How far along are companies with AI transformation in 2026?

Deployed is the mode; embedded is rare. In the Open Future Forum rooms, 71 percent of the largest finance room runs an AI tool (base 185), and 9 of 38 in the growth room run agents in production across the business. Externally, McKinsey finds only 7 percent of firms have fully scaled AI.

Who signs off on AI transformation spend?

In the Open Future Forum finance rooms, the CEO is the most named signer of a new AI purchase at 47 percent, then the CFO or finance at 25 percent and the CIO or CTO at 23 percent (base 87, any-mention). Founders selling in target a different seat: the CIO or CTO at 43 percent (base 92).

Is AI transformation reducing headcount?

The early signals are indirect: 17 percent of the finance rooms fund this year's AI budget with money that would have gone to headcount (base 87), and Gartner finds finance leaders' expected headcount growth falling from 6 to 2 percent. The Headcount Posture metric measures the decoupling directly from the next edition.

How is this different from AI adoption surveys?

Adoption surveys count usage across large anonymous samples. This report reads the transformation markers themselves, spend source, headcount posture, handed-over work, and governance, at the operator level, in one community, tracked over editions, with the base on every figure.

What We Will Measure

The answers in hand today are demand, composition, and the cross-lane instrument reads above. The flagship layer arrives with the question below, which is new: it has not yet been fielded anywhere, and this edition says so plainly. It enters the registration flow at upcoming events across all lanes.

The Flagship Metric: the AI Transformation Index

Question (operating executives only, about the function they lead): AI in the function you lead today is: still being explored / running in pilots / deployed in one or two workflows / embedded in how the function runs, changing its cost structure or hiring plan / not material.

The Index is the combined share choosing the two live stages, deployed in one or two workflows plus embedded, reported as a single percentage with the full distribution beneath it, tracked edition over edition, overall and by lane. Until it clears the 40-response role-tagged floor, the buying-stage question (base 185) is reported as the seed series and closest proxy, clearly labeled, and never presented as the Index itself.

Supporting metrics

- Transformation Funding. This year's AI budget is mostly: net-new / reallocated from other software / money that would have been headcount / no budget yet. The spend marker, already seeded at base 87.

- Headcount Posture. Over the next 12 months the team will: grow / hold flat with growing scope / hold flat with flat scope / shrink. The decoupling marker.

- Process Readiness. The workflows AI would take over are documented well enough to hand off: yes / partly / no. The handed-over-work marker, measured before the handover.

- Governance Read. An inventory of live AI tools and data connections exists: yes / partial / no. The governance marker, already seeded directionally in the security room.

The instrument

Core, every edition, operating executives only: the flagship question and the four supporting metrics. Rotating deeper set, one or two per edition: compression of a named piece of work in before-and-after bands; agents in production, yes or no, and in which workflow; the share of AI spend on usage or outcome pricing; and whether an AI purchase has been canceled and what happened to its access. One trade is stated in the open: publishing the instrument invites priming, and holding it back invites distrust; this program publishes it.

How It Runs

Sample and Honesty

The figures describe the Open Future Forum community, a selective sample drawn from the finance, security, growth, founder, and investor rooms rather than a probability sample of all enterprises, and they are not presented as one. Every headline figure states its base, no headline is published below 40 role-tagged responses, and early editions are framed as directional reads of what the operators in this community are doing. A smaller claim, fully backed, beats a larger one that invites the obvious critique.

Assets Each Edition Produces

- The published report, for the site and the newsletter, written to be quoted and cited.

- A one-page summary graphic led by the AI Transformation Index and the funding read.

- A short methodology note, so the report is citable as a source.

- Lane cuts, sent to each room's list as its own short piece.

- “The AI Transformation Report reads how far the operating executives in the Open Future Forum community have moved AI from pilots into the way their functions run, on four markers: spend, headcount, work, and governance.”

- “In the Open Future Forum rooms in 2026, 71 percent of the largest finance room already runs an AI tool (base 185), while 46 percent of finance respondents fund this year's AI budget mostly with net-new money (base 87).”

- Once the flagship clears the floor, always cite with the base: “Among the operating executives in this edition (n = X), Y percent say AI is deployed in one or two workflows or embedded in how their function runs.”

Suggested Citation and Versioning

Cite as: Open Future Forum, The AI Transformation Report, Edition 1, July 2026.

The report is a recurring series, released as the data supports rather than on a fixed schedule. Each edition carries an edition number and a date, lives at a stable URL, and supersedes nothing. Prior editions stay published so the AI Transformation Index line can be tracked. Short handle for repeat reference: the AI Transformation Index.

Methodology and Disclosure

Methodology Note

The AI Transformation Report is produced by Open Future Forum. Demand-context figures are drawn from application records for Open Future Forum events; they are reported as distinct-applicant floors by lane and may include individuals who apply to more than one event. Invitation outreach that did not become an application is excluded from every count, and application is not attendance. Instrument figures are drawn from questions embedded in the event application flow; they are application-stage answers, reported with the response base stated and a minimum of 40 role-tagged responses per published headline figure. Reads below that floor are labeled directional. The rooms are role-mixed: they include founders, investors, engineers, and advisors alongside the operating executives, so room-level figures describe who was in the room, and role-tagged cuts are shown where they exist. This report is cross-lane by design: figures are drawn from the finance, security, growth, founder, and investor rooms, with the lane stated on every figure. Multi-select questions are reported any-mention and can sum past 100 percent; each figure states its conventions on its face. The flagship transformation-stage question is entering the field at upcoming events; until it clears the floor, the buying-stage read (base 185) is the seed series and closest proxy. External benchmarks are attributed and used only for context.

Independence and Disclosure

- Open Future Forum runs the events and sells sponsorships. Murray Newlands does fractional advisory work with AI companies, disclosed because this edition covers the market those companies sell into.

- Sponsors do not see, shape, or approve the questions, the analysis, or the findings.

- The report never ranks, scores, or recommends specific vendors or products. It reports aggregate behavior only.

- The findings are the community aggregate. The report is not a lead-generation instrument, and respondent contact data is never passed to sponsors.

This statement runs in every edition.

About Our Events and Open Future Forum

Open Future Forum convenes executives, founders, and investors across a program of dinners, panels, and gatherings, held in partnership with leading institutions and co-chaired with senior industry leaders. These institutions partner on the events; they do not endorse or contribute to this report, which is editorially independent.

Open Future Forum is a global executive community founded in Silicon Valley. Its network reaches tens of thousands of executives and investors worldwide. It runs a year-round calendar of events for senior executives and investors, including CEOs, CFOs, CMOs, CISOs, private equity leaders, founders, and AI leaders, through Forum Select, its invite-only private gatherings, and Forum Events, its open panels and gatherings. Beyond events, Open Future Forum convenes peer groups and executive boards and publishes original research built on first-party survey and qualitative data from its executive network. The AI Transformation Report is part of its operator-level research program.

Sources

First-party sources: instrument questions embedded in the application flow for Open Future Forum events in 2026, spanning the finance rooms (185 responses on buying stage; 87 combined on budget source, sign-off, blocker, and return window), the security rooms (26 instrument responses, 10 from security leaders), the founder events (92 buyer and pricing responses, 83 charging), the go-to-market room (38 stage responses), and the investor gathering (20 responses); plus application records across the twelve events in the July 2026 pull.

Third-party figures are drawn from the sources below. Primary external data sources link to the original reports; other sources link to the publisher, where the specific release can be found.

- Menlo Ventures. 2025: The State of Generative AI in the Enterprise. Enterprise AI spend, growth rate, and production conversion. menlovc.com

- a16z. How 100 Enterprise CIOs Are Building and Buying Gen AI in 2025. Innovation-budget shift and spend growth. a16z.com

- MarketsandMarkets. Agentic AI Security Market, Global Forecast to 2032. marketsandmarkets.com

- MIT. The GenAI Divide: State of AI in Business 2025, MIT Project NANDA. Pilot outcomes and measurable profit. mit.edu

- S&P Global Market Intelligence. Survey data on companies abandoning AI initiatives. spglobal.com

- McKinsey & Company. Research on AI scaling, EBIT impact, and adoption by industry. mckinsey.com

- Gartner. Forecasts on agentic project cancellations, finance headcount expectations, and software pricing. gartner.com

- Boston Consulting Group. BCG AI Radar 2026: survey of 2,360 executives including 640 CEOs. bcg.com

- Wharton Human-AI Research and GBK Collective. Accountable Acceleration: Gen AI Fast-Tracks Into the Enterprise, about 800 senior leaders at large US companies, October 2025. ai.wharton.upenn.edu

- KPMG. AI Quarterly Pulse Survey, US C-suite leaders at $1 billion-plus organizations. Agent deployment, validation, and AI cost visibility. kpmg.com

- US Census Bureau. Business Trends and Outlook Survey and AI supplement, nationally representative AI use at US businesses. census.gov

- Bloomberg. Reporting on Uber's monthly per-tool caps on agentic coding spend. bloomberg.com

- Deloitte. Enterprise AI adoption by industry. deloitte.com

- NVIDIA. State of AI 2026. Industry adoption and return. nvidia.com

- Intercom. Per-resolution pricing for AI customer service. A vendor's own pricing, cited as a market signal, not a benchmark. intercom.com

External benchmarks are used for context only. They are not affiliated with this report and do not endorse it.

This report is published by Open Future Forum for general information and research purposes only. It is not legal, financial, investment, tax, accounting, or other professional advice, and it should not be relied on as such. Nothing in it is a recommendation to buy, sell, or hold any security, product, or service, or to adopt any particular budget, vendor, or course of action. Figures drawn from Open Future Forum events are early, directional reads on small and self-selected samples, and figures from third parties belong to the organizations cited and are used for context. Readers should do their own research and consult their own qualified advisors. Open Future Forum makes no warranty as to the accuracy or completeness of this report and accepts no liability for any action taken in reliance on it.

© 2026 Open Future Forum. All rights reserved. The AI Transformation Report and the AI Transformation Index are works of Open Future Forum. No part may be reproduced or redistributed for commercial purposes without permission. Quotation for journalism, research, and commentary is welcome with attribution to Open Future Forum. Third-party names and marks belong to their owners.

Compare Notes on Your Own Transformation

Private, off-the-record gatherings for executives navigating AI budgets, headcount, and governance. No vendors. No agenda.